Young people need practical money experience to build lasting financial skills. Traditional banking often keeps children separate from real financial decisions until they turn 18. The greenlight debit card approach changes this by giving kids and teens controlled access to money while parents maintain oversight. This combination lets young people make choices, see consequences, and develop habits before they face high-stakes financial situations.

How Greenlight Debit Cards Work

A greenlight debit card is a spending tool designed for minors with built-in parental controls. Parents fund the card, set spending limits, and monitor transactions through a companion app. The child receives a physical card linked to their parent's account but operates it independently within the established boundaries.

The system differs from traditional bank accounts in several ways. Parents can control where the card works by enabling or disabling spending categories like restaurants, gas stations, or online shopping. They receive instant notifications when their child makes a purchase. The child sees their balance update immediately and can track their spending history.

Core Features That Build Skills

Greenlight debit products typically include these elements:

- Spending controls that let parents approve or block merchant types

- Real-time alerts showing every transaction as it happens

- Savings goals with visual progress tracking

- Chore and allowance automation for consistent funding

- Investment accounts for older teens (on some plans)

According to FinanceBuzz's comprehensive analysis, these features help families create structured learning experiences around everyday purchases.

Comparing Greenlight Debit to Traditional Banking

Traditional bank accounts for minors require a parent as joint owner. This setup gives parents full visibility but offers less granular control over individual transactions. The child may have limited independence until they reach legal adulthood.

| Feature |

Greenlight Debit |

Traditional Bank Account |

| Parental Controls |

Category-level spending limits |

View-only or full access |

| Real-Time Monitoring |

Instant purchase notifications |

Transaction history review |

| Minimum Age |

Varies by provider |

Often 13-16 with parent |

| Monthly Fees |

$4.99-$14.98 typical |

Often waived for minors |

| Learning Tools |

Built-in tasks and goals |

Basic statements |

Greenlight's comparison guide explains how their model emphasizes financial education over simple account access. This philosophy aligns with modern approaches to youth financial education that prioritize hands-on practice.

What Parents Can Control

The greenlight debit framework gives parents several intervention points. They can set daily or weekly spending caps that reset automatically. When a child tries to buy something outside their allowed categories, the transaction declines. Parents can send money instantly when needed or schedule regular allowance deposits.

Some systems let parents require approval for purchases over a certain amount. A teenager might have freedom to spend $20 without permission but need to request approval for anything larger. This graduated approach builds decision-making skills while maintaining safety nets.

How Young People Learn Through Use

Financial education works best when connected to real experiences. A child who receives $10 and must decide between spending it now or saving for a $50 item learns more than one who simply reads about delayed gratification.

The greenlight debit model creates these learning moments naturally. When the balance hits zero, the child can't make another purchase until they receive more money. This immediate consequence teaches budgeting faster than theoretical discussions.

Practical Scenarios That Build Understanding

Consider a 14-year-old who wants new headphones costing $80. With a greenlight debit card, they can:

- Check their current balance

- Set up a savings goal with a deadline

- Track weekly allowance deposits

- Resist smaller impulse purchases

- Celebrate when they reach the target amount

Each step reinforces a financial concept. The visual progress toward the goal makes abstract ideas concrete. When they finally make the purchase, they understand the tradeoff between immediate wants and planned goals.

Finder's review highlights user experiences where children developed saving habits within months of starting to use these cards. The key seems to be the combination of personal ownership and visible consequences.

Earnings and Financial Responsibility

The greenlight debit system works particularly well when young people earn their card balance rather than simply receiving it. Connecting money to effort creates stronger financial awareness than allowances alone.

Many families link card funding to completed tasks. A child might earn $5 for mowing the lawn or $2 for completing homework without reminders. The money appears on their greenlight debit card immediately after parents approve the work.

Building the Work-Money Connection

This earn-and-spend cycle mirrors adult financial life. Just as adults work to receive paychecks, young people complete responsibilities to fund their cards. The difference is the controlled environment where mistakes have limited impact.

Modern platforms like micro-learning platforms extend this concept by paying young people for completing educational tasks. Learners might earn money for finishing math practice, writing book reports, or learning new skills. The earnings go directly to their debit card, creating a tangible link between learning and financial reward.

This approach addresses a common challenge with greenlight debit cards. When parents simply deposit allowances with no connection to behavior or achievement, children may not develop strong money values. Tying deposits to completed work or learning makes the financial lessons more powerful.

Fee Structures and Value Assessment

Most greenlight debit programs charge monthly subscription fees ranging from $4.99 to $14.98 depending on features. Higher tiers typically include investment accounts, higher interest rates on savings, and family perks like purchase protection.

Parents should weigh these costs against the educational value. A $5 monthly fee equals $60 annually. Compare this to the cost of financial mistakes a young adult might make without preparation, such as overdraft fees, late payment charges, or impulse purchases on uncapped credit cards.

Breaking Down Monthly Costs

Basic greenlight debit plans typically offer:

- One parent account with up to five child cards

- Spending controls and real-time alerts

- Savings goals and balance tracking

- Basic customer support

Premium plans may add:

- Investment account access for teens

- Higher savings interest rates

- Cell phone protection or purchase insurance

- Priority customer service

- Custom card designs

BestMoney's review examines whether these premium features justify the additional cost for most families. The conclusion often depends on whether older teens will use investment features and whether parents value the added protections.

Privacy and Security Considerations

Greenlight debit cards carry similar security protections as adult debit cards. The accounts are typically FDIC-insured, meaning deposits are protected up to $250,000 if the partner bank fails. The cards use chip technology and can be locked instantly through the app if lost or stolen.

Parents maintain ultimate control over the account. They can view every transaction, freeze the card, or adjust limits at any time. The child cannot change these settings without parent approval.

Teaching Digital Safety

Using a greenlight debit card also creates opportunities to discuss online security. Young people learn to:

- Recognize secure websites before entering card numbers

- Avoid sharing card details through text or email

- Monitor statements for unauthorized charges

- Report suspicious activity immediately

- Use strong passwords for account access

These digital literacy skills extend beyond financial management. As detailed in discussions of 21st century learning skills, understanding digital security is fundamental to modern capability.

Integration with Broader Financial Education

A greenlight debit card alone does not create financial literacy. It's a tool that becomes educational when combined with intentional teaching. Parents should discuss transactions, explain why certain limits exist, and help children analyze their spending patterns.

Some families hold weekly money meetings where they review card activity together. They might discuss questions like: What did you spend money on this week? Do you wish you had made different choices? How close are you to your savings goal?

Connecting Cards to Life Skills

Schools that teach life skills often incorporate financial tools into their curriculum. A classroom might use greenlight debit cards as part of an economics unit, with students earning card balances for academic work and making spending decisions within a simulated economy.

This integration makes abstract financial concepts tangible. When a child earns $10 for completing a project and must decide whether to spend it or save for a class reward, they experience budgeting firsthand.

| Learning Goal |

Greenlight Debit Application |

Reinforcement Activity |

| Budgeting |

Weekly spending limit |

Track and categorize expenses |

| Delayed Gratification |

Savings goals with visual progress |

Compare short vs. long-term purchases |

| Earning |

Card funding tied to tasks |

Calculate hourly value of different jobs |

| Comparison Shopping |

Real purchases across merchants |

Research before buying, check prices |

| Digital Literacy |

Online transaction security |

Identify safe vs. unsafe websites |

Age Considerations and Developmental Stages

The appropriate age to introduce a greenlight debit card varies by child. Most providers allow cards for children as young as six, but readiness depends on maturity and mathematical understanding.

Younger children (ages 6-9) may benefit from simple earn-and-spend experiences. They can grasp that completing a task earns money and that purchases reduce their balance. Complex budgeting and long-term planning may exceed their developmental stage.

Adjusting Complexity by Age

Pre-teens (ages 10-12) can handle more sophisticated concepts. They can maintain multiple savings goals, track spending across categories, and begin to understand percentage-based concepts like interest or discounts.

Teenagers (ages 13-18) should graduate to near-adult financial responsibility. They might manage clothing budgets, save for larger goals like a car, or even contribute to household expenses. The greenlight debit card becomes a bridge to full financial independence rather than a training tool.

WalletGrower's review suggests starting with highly supervised use and gradually reducing oversight as the child demonstrates responsible decision-making. This mirrors how parents approach other areas like internet use or driving privileges.

Prepaid vs. Debit Classification

Some confusion exists about whether greenlight cards are prepaid or debit products. Greenlight clarifies that their cards function as debit cards connected to FDIC-insured accounts rather than traditional prepaid cards.

The distinction matters for several reasons. Prepaid cards often carry more fees, offer less fraud protection, and don't build banking relationships. Debit cards linked to accounts provide better security and create pathways to future banking services.

For parents, this means greenlight debit cards can serve as legitimate banking education rather than just temporary spending tools. The child learns to check balances, understand account activity, and manage a financial account rather than simply loading and spending a prepaid balance.

When Greenlight Debit Makes Sense

These cards work best for families committed to active financial education. Parents who lack time for regular money conversations may find the card provides limited value beyond convenience.

Ideal candidates include:

- Families wanting structured allowance systems

- Parents teaching budgeting through real experience

- Households with children earning money through tasks

- Families preparing teens for financial independence

- Parents seeking alternatives to cash handouts

The cards may be less valuable for:

- Very young children (under age 6-7)

- Families preferring cash-based teaching methods

- Parents unwilling to pay monthly fees

- Situations where children have minimal spending opportunities

Kids' Money's personal account of using greenlight debit cards describes both successes and limitations, helping families set realistic expectations.

Alternative Approaches to Youth Banking

Greenlight is one of several companies offering youth debit cards. Competitors include GoHenry, FamZoo, BusyKid, and Copper. Each has different fee structures, features, and age ranges.

Some families prefer traditional bank accounts with debit cards designed for minors. North State Bank's greenlight debit card represents a hybrid approach where established banks partner with fintech companies to offer enhanced features.

Evaluating What Works for Your Family

The best debit card for kids depends on family goals, child age, and budget. Consider these factors:

- Monthly fee tolerance

- Desired level of parental control

- Whether multiple children need cards

- Investment or savings features

- Customer service quality

- Ease of use for both parents and children

Some families rotate between different products as their children age, starting with highly controlled options and graduating to more independent accounts as teens demonstrate responsibility.

Real-World Impact on Financial Behaviors

Research on youth financial education shows mixed results for classroom-only approaches. Young people often forget theoretical knowledge when they don't apply it regularly. Tools like greenlight debit cards address this by creating continuous practice opportunities.

A teenager who manages $50 weekly through a debit card makes dozens of financial decisions each month. They experience regret from impulse purchases, satisfaction from reaching savings goals, and the discipline of waiting when funds run out. These experiences build financial intuition that lectures cannot create.

1AND1 Life's review discusses how consistent use over months can shift spending patterns and increase savings rates among children and teens using these cards. The key appears to be sustained engagement rather than one-time lessons.

Measuring Success

Parents can track several indicators of financial growth:

- Savings rate: What percentage of deposits does the child save vs. spend?

- Impulse control: How often do they request emergency funds after overspending?

- Goal completion: Do they reach savings targets or abandon them?

- Spending awareness: Can they accurately estimate their balance without checking?

- Category patterns: Are they making conscious choices about where money goes?

Improvement in these areas suggests the greenlight debit card is functioning as an educational tool rather than just a payment method.

Parent-Child Communication Around Money

The greatest value of greenlight debit systems may be the conversations they enable. When parents can see transaction histories, they have concrete examples for discussing financial choices.

Instead of abstract discussions about "being responsible with money," parents can ask specific questions. Why did you buy that app? How did you decide between those two items? What would you do differently next time?

These discussions work best when framed as collaborative problem-solving rather than criticism. The goal is helping the child develop their own financial judgment, not enforcing rigid rules indefinitely.

Creating Teaching Moments

Every declined transaction is a learning opportunity. When a child tries to buy something they cannot afford, parents can discuss budgeting, prioritization, and delayed gratification. When a child reaches a savings goal, parents can celebrate and discuss what strategies helped them succeed.

Regular reviews of spending patterns help children recognize their own habits. They might notice they spend more on weekends or that small purchases add up quickly. This self-awareness forms the foundation for long-term financial capability.

Connecting to Broader Life Skills

Financial management sits within a larger framework of personal capability. Young people who learn to budget, plan, and make tradeoffs with money often transfer those skills to other areas like time management, academic planning, and career preparation.

Programs that combine financial tools with broader skill development create more comprehensive growth. When a young person earns greenlight debit card deposits by completing educational tasks, they simultaneously build money skills, subject knowledge, and work habits.

This integrated approach reflects how adults actually use financial skills. We don't budget in isolation; we budget to achieve life goals, support careers, and enable experiences we value. Teaching young people to connect money management to their larger aspirations creates more meaningful learning than focusing on finances alone.

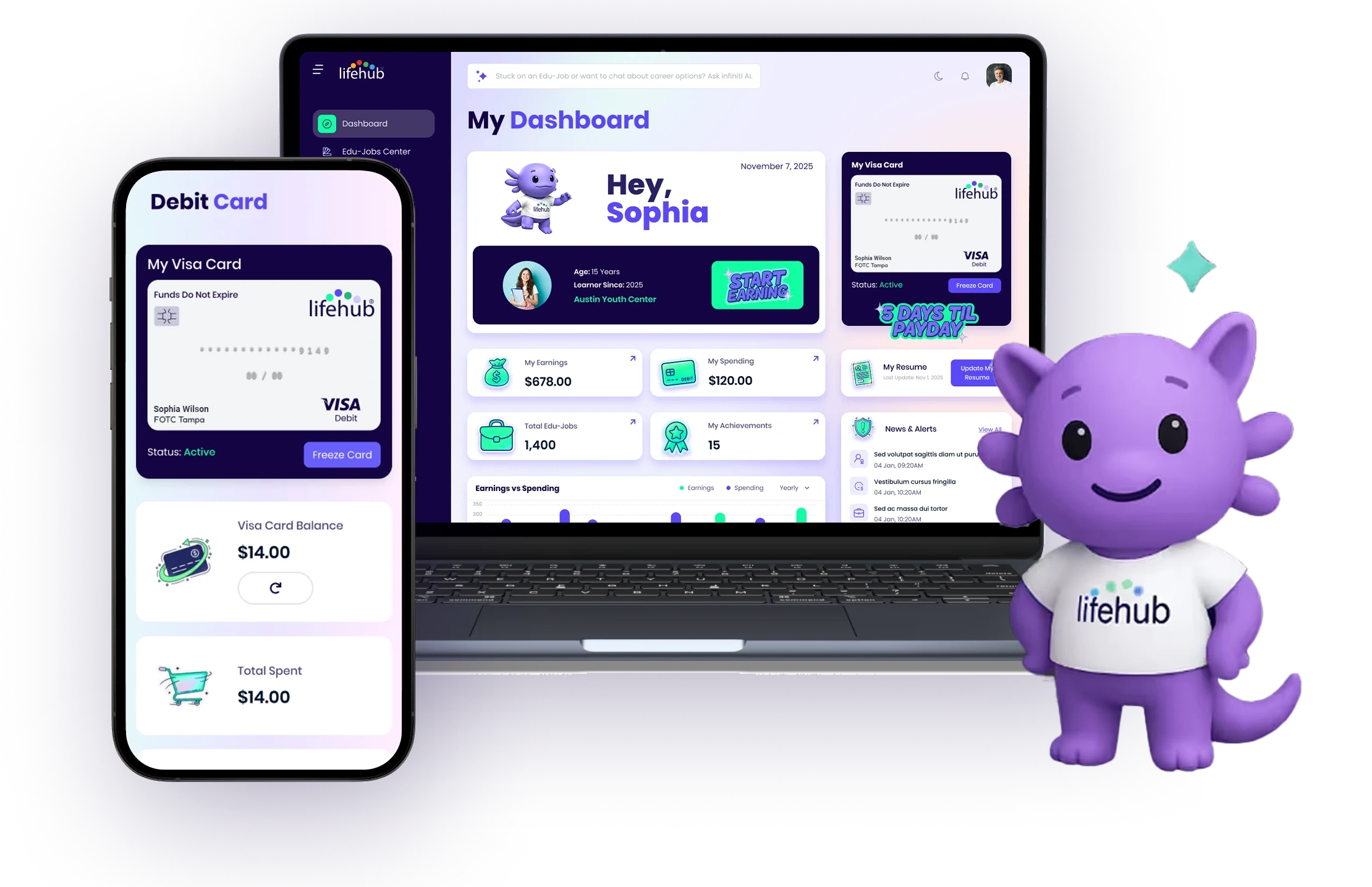

Greenlight debit cards can provide valuable hands-on financial education when families use them intentionally. The combination of controlled independence and real consequences creates learning opportunities that theoretical instruction alone cannot match. If you want to connect financial growth with broader skill development, Life Hub offers an approach where young people earn real money deposited to a Visa debit card by completing educational micro-tasks across subjects from math and reading to financial literacy and career skills. This creates the powerful combination of learning through action and seeing immediate, tangible rewards for effort.

.avif)

.png)

.svg)

.svg)