Related Content

No items found.

Learning money is one of the most valuable skills young people can develop, yet it remains surprisingly absent from many educational experiences. In 2026, financial decisions affect every aspect of life, from daily purchases to career choices, making early money education more important than ever. The gap between what schools teach and what young people need to know about finances continues to widen, leaving many families searching for better solutions.

Young people learn money concepts most effectively when they can practice with real situations. Reading about budgeting or saving differs significantly from actually earning, deciding how to spend, and experiencing the consequences of those choices. Teaching young people about money becomes more impactful when it connects to their immediate lives.

Traditional classroom approaches often present financial concepts in abstract ways. A textbook lesson about compound interest may seem irrelevant to a 12-year-old with no income or savings account. Research shows that financial literacy education improves when learners can apply concepts immediately rather than storing them away for future use.

The disconnect becomes clear when young people reach adulthood. Many enter college or their first jobs without understanding paycheck deductions, credit card interest, or basic budgeting. They learned the theory but never practiced the skills.

Earning money transforms financial education from abstract to concrete. When young people work for their income, even through small tasks, they develop a different relationship with money than receiving allowances provides.

Key benefits of earned income for learning money:

A micro-learning platform approach lets young people take on age-appropriate financial tasks. They complete specific assignments, get compensated, and decide how to use their earnings. This cycle reinforces multiple money concepts simultaneously.

Parents serve as the primary money educators, whether they plan to or not. Children watch how adults handle purchases, discuss bills, and react to financial stress. According to research on financial education, kids learn more about money from family experiences than formal instruction.

Parents can strengthen learning money by:

The challenge for many parents involves finding structured ways to provide these experiences. Daily life gets busy, and teaching moments may pass unnoticed without intentional planning.

Learning money encompasses more than understanding coins and bills. A comprehensive approach covers multiple interconnected skills that learners will use throughout their lives.

Money Skill AreaWhat It IncludesWhy It MattersEarningWork value, compensation, task completionBuilds work ethic and income understandingSpendingNeeds vs. wants, price comparison, purchase decisionsDevelops consumer awareness and decision-makingSavingGoal-setting, delayed gratification, emergency fundsCreates financial security habitsSharingCharitable giving, helping others, community impactBuilds values and perspective

Young learners need exposure to concepts that reflect modern financial reality. Digital payments, online purchases, subscription services, and app-based banking represent their financial future. Youth financial education must address these realities alongside traditional concepts.

A 2026 approach includes:

Effective financial education requires more than information delivery. Young people need structured opportunities to practice money skills in safe environments where mistakes carry limited consequences.

Task-based approaches connect learning money with skill development across multiple areas. When a young person completes a research project about local businesses and earns payment for quality work, they experience:

This integration makes financial learning feel relevant rather than isolated. Schools that teach life skills recognize that money management connects to career readiness, personal responsibility, and goal achievement.

Learning money should evolve as young people develop. A progression might look like:

Ages 6-9:

Ages 10-13:

Ages 14-18:

Parents can explore shopping experiences with younger children to build foundational concepts. These early experiences shape attitudes that persist into adulthood.

Technology changes how young people interact with money and how they can learn financial skills. Mobile apps, digital wallets, and online banking have become standard tools, making digital literacy essential for financial success.

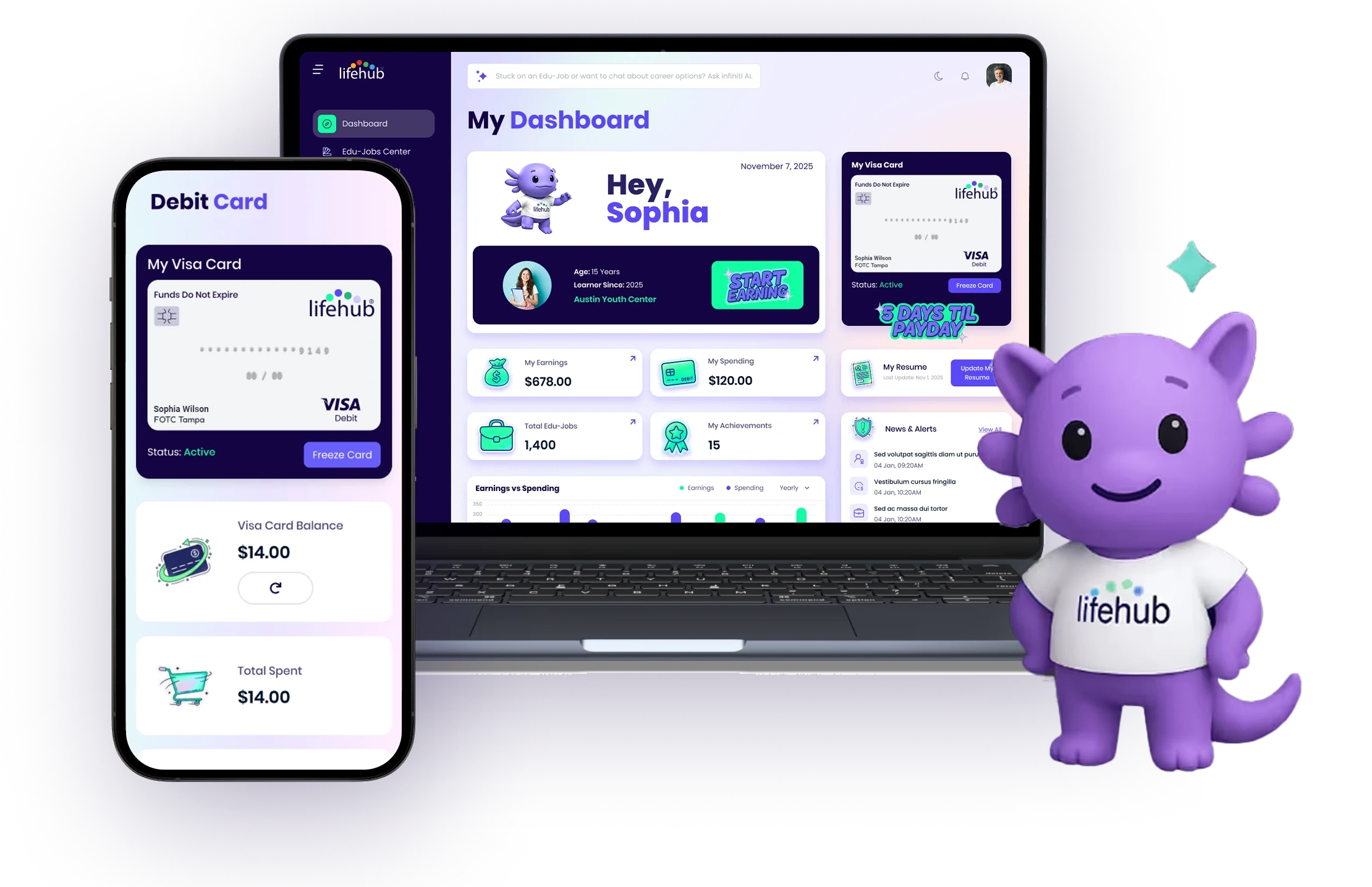

The best debit card for kids combines financial access with learning features. Young people can see their balance, track spending, and make decisions while parents maintain appropriate oversight. This hands-on experience builds confidence and competence.

Benefits of technology-enabled financial learning:

Technology also enables new approaches to earning. Digital platforms can connect young learners with age-appropriate tasks, verify completion, and deposit earnings directly. This streamlined process removes barriers that previously made earning opportunities difficult for younger age groups.

Learning money shouldn't exist in isolation from other educational goals. The most effective approaches integrate financial concepts with academic subjects, career exploration, and personal development.

Financial literacy naturally connects to:

When financial learning integrates with AI education for kids, young people can explore how technology affects banking, investments, and financial decision-making. They learn both financial concepts and digital literacy simultaneously.

Understanding money connects directly to career development. Young people who learn about different income levels, work requirements, and compensation structures make more informed educational and career choices.

Exploring careers through paid tasks helps learners:

This practical approach to youth financial education prepares learners for workforce entry while building money management skills.

Every young person deserves access to quality financial education, regardless of family income or school resources. The challenge involves creating scalable solutions that work across different contexts.

Traditional barriers include:

Modern solutions address these challenges through structured programs. When organizations, schools, or companies sponsor learning opportunities, they remove the barrier of family funding while providing young people with genuine earning experiences.

Confidence with money develops through successful experiences. A young person who earns their first payment, saves toward a goal, and makes a planned purchase builds self-efficacy that extends beyond finances.

Steps to build financial confidence:

Teaching kids about wealth requires balancing support with independence. Young people need opportunities to make real decisions and experience natural consequences.

Unlike academic subjects with clear assessment methods, measuring financial literacy presents unique challenges. Test knowledge may not reflect actual money management capability.

Effective assessment for learning money includes:

Assessment TypeWhat It MeasuresExampleKnowledge testsUnderstanding of conceptsDefining budget, interest, investmentPerformance tasksApplication of skillsCreating a savings plan for a goalReal transactionsActual money decisionsTracking spending over a monthSelf-reflectionAwareness and growthJournaling about financial choices

The most meaningful measure comes from observable behavior change. Does the young person make more thoughtful purchase decisions? Do they save toward goals? Can they explain their financial reasoning?

Research continues to demonstrate that financial education in youth creates lasting benefits. Young people who develop strong money skills show better outcomes in multiple life areas.

Early learning money correlates with:

These outcomes matter because financial struggles affect mental health, relationships, career choices, and overall wellbeing. Studies on financial literacy education show causal effects on financial health, supporting investment in youth programs.

The transition to adult financial independence challenges many young people. Those with practical money experience navigate this change more successfully than those learning everything at once.

Skills that support financial independence include:

Starting these skills early through incremental practice creates competence before high stakes decisions arrive.

Learning money is an ongoing process that extends through childhood, adolescence, and into adulthood. The foundation built during younger years shapes lifelong financial behaviors and outcomes. Parents, educators, and communities all play important roles in providing learning opportunities and support.

The key lies in making financial education practical, relevant, and connected to real experiences. When young people earn, spend, save, and make decisions with actual money, they develop both skills and confidence. These experiences prepare them not just for financial tasks but for the independence and responsibility of adulthood.

Building strong money skills early creates advantages that compound throughout life. Young people need practical ways to earn, manage, and learn from real financial experiences in safe, supportive environments. Life Hub connects learners with paid educational tasks across financial literacy, career exploration, academics, and digital skills, letting them earn real money while building practical capabilities. Each completed task strengthens both knowledge and confidence, creating a direct link between effort and reward that motivates continued growth.

Whether you're parents, or a homeschool family, Life Hub is your partner to help you

raise super strong kids.

Turning high value micro-learning into real-world cash and non-cash rewards with tokenization.

.svg)

Electus Global Education Co, Inc. has received support from The American Heart Association Social Impact Funds.

.svg)