Parents face a common challenge: teaching children practical money skills in a world that increasingly relies on digital payments. The greenlight prepaid card has emerged as one solution, offering families a way to introduce banking concepts while maintaining oversight. This debit card designed for children and teens allows parents to monitor spending, set limits, and create learning moments around everyday financial decisions. Understanding how these tools work can help families choose the right approach for building lasting money skills.

What Makes the Greenlight Prepaid Card Different

The greenlight prepaid card operates as a family account system that includes separate cards for each child. Parents control the main account and can instantly transfer funds to their children's cards through a mobile app. This structure lets young people practice spending while adults retain full visibility and control.

Core Features and Account Structure

Each family subscription includes cards for up to five children. Parents manage everything through a central dashboard that shows transactions in real time. The system allows you to set spending limits by category, such as groceries, entertainment, or restaurants.

Key capabilities include:

- Instant money transfers from parent to child accounts

- Spending notifications for every transaction

- Category-based spending controls

- Automatic allowance scheduling

- Savings goals with parent-matching options

- Basic investing features for older teens

The card works anywhere Mastercard is accepted. Children can use it for online purchases, in-store shopping, or ATM withdrawals within parent-approved limits.

Pricing Structure and Monthly Costs

The greenlight prepaid card operates on a subscription model with several tiers. The basic plan costs $5.99 per month and covers core features like spending controls and allowance automation. This fee applies to the entire family regardless of how many children use cards.

| Plan Type |

Monthly Cost |

Main Features |

| Greenlight |

$5.99 |

Spending controls, allowance, savings goals, chore tracking |

| Greenlight + Invest |

$9.98 |

Everything in basic plan plus custodial investing account |

| Greenlight Max |

$14.98 |

All features plus identity theft protection, cell phone coverage |

Additional fees may apply for specific transactions. ATM withdrawals beyond one free withdrawal per month cost $2.50 each. Replacement cards cost $3.50. The system does not charge overdraft fees because spending is limited to available funds.

Finder's detailed review breaks down these costs and compares them to similar services. Some families find the monthly fee worthwhile for the convenience and educational features. Others prefer no-fee alternatives depending on their specific needs.

Understanding the Total Cost of Ownership

When evaluating any prepaid card system, consider both obvious and hidden costs. The subscription fee is clear, but transaction fees can add up if children frequently withdraw cash or if you need to replace lost cards.

Compare this to the cost of alternative approaches. Some families manage allowances through cash or basic bank accounts at no monthly charge. The value comes from features like automated systems, spending insights, and built-in educational tools that may save time and create more teaching moments.

Teaching Opportunities Through Managed Spending

The greenlight prepaid card creates daily chances to discuss money decisions. When a child makes a purchase, both parent and child receive instant notifications. This visibility opens conversations about whether the purchase aligned with priorities and goals.

Building Decision-Making Skills

Young people learn through repetition and feedback. Having their own card lets them practice making choices with real consequences. If they spend their allowance too quickly, they experience the natural result of having to wait until the next payment.

Parents can adjust controls as children demonstrate responsibility. A middle schooler might start with strict category limits. Over time, those restrictions can loosen as they show good judgment. This gradual release of control mirrors the path toward full financial independence.

Practical learning moments include:

- Comparing prices before purchasing

- Choosing between immediate wants and savings goals

- Understanding that digital money is still real money

- Managing a limited budget across different needs

- Experiencing the satisfaction of reaching a savings target

Research shows cash rewards enhance educational outcomes when tied to learning activities. The same principle applies to money management skills developed through hands-on practice.

Savings Features and Goal Setting

The platform includes tools to help children save toward specific objectives. Kids can create named savings goals with target amounts and deadlines. The interface shows progress visually, making abstract future rewards more concrete.

Parents can offer matching contributions to incentivize saving. For example, you might match 50 cents for every dollar your child saves toward a bicycle. This introduces the concept of employer retirement matches or other matched savings programs they'll encounter later in life.

Interest Earning Potential

The greenlight prepaid card offers interest on savings balances. Rates vary based on the plan level and can change over time. As of 2026, the standard plan offers up to 2% annual percentage yield on savings.

While the interest earnings won't be substantial on typical child savings amounts, the concept matters. Children see their money grow without additional effort, introducing the power of compound interest and passive income.

Limitations and Common Concerns

No financial product suits every family perfectly. The greenlight prepaid card has specific drawbacks worth considering before subscribing.

Consumer reviews on ConsumerAffairs highlight recurring complaints. Some users report customer service challenges, particularly with account access issues or disputed charges. Others find the monthly fee excessive for features they don't fully use.

Technical and Access Issues

The system relies entirely on smartphone apps for management. Parents without reliable internet access or who prefer not to manage finances through phones may find this limiting. The platform occasionally experiences technical glitches that temporarily prevent transactions or transfers.

Common frustrations include:

- Delayed card activation taking several weeks

- App connectivity problems blocking fund transfers

- Limited phone support during account issues

- Difficulty canceling subscriptions or getting refunds

- Restrictions on international use

Some parents also question whether app-based money management truly prepares children for adult banking. The simplified interface may not reflect the complexity of actual bank accounts, credit cards, and financial institutions they'll navigate later.

Comparing Alternative Approaches to Youth Banking

Several competitors offer similar services with different features and pricing. FamZoo charges $5.99 per month for up to four cards and emphasizes flexible customization. BusyKid costs $4.00 per month and focuses heavily on chore-based allowances. Step offers a no-fee option with fewer parental controls but no subscription cost.

| Service |

Monthly Fee |

Key Differentiator |

| Greenlight |

$5.99-$14.98 |

Comprehensive features, investing option |

| FamZoo |

$5.99 |

Highly customizable, prepaid approach |

| BusyKid |

$4.00 |

Chore tracking emphasis, lower cost |

| Step |

$0 |

No fees, fewer parental controls |

| GoHenry |

$4.99 |

Strong educational content, spending limits |

BestMoney's comparison evaluates these options based on fees, features, and user experience. The right choice depends on your family's priorities. Younger children might benefit from more restrictive controls while older teens may prefer greater independence.

Traditional Banking Alternatives

Many credit unions and community banks offer free youth checking or savings accounts. These typically require parent co-ownership until the child reaches 18. They may lack sophisticated app features but introduce young people to actual banking institutions they'll use as adults.

Some families combine approaches. They might use a basic savings account for long-term goals while employing a prepaid card for spending money. This separation can reinforce the difference between saving and spending.

Privacy and Security Considerations

The greenlight prepaid card collects significant data about family spending patterns. The company's privacy policy describes how they use and share this information. Parents should review these terms to understand what data collection they're authorizing.

Security features include card locking, transaction alerts, and the ability to instantly freeze any card through the app. If a child loses their card, you can prevent unauthorized use immediately while waiting for a replacement.

Teaching Digital Safety

Using a prepaid card creates chances to discuss online security. Young people learn to:

- Protect card numbers and PINs

- Recognize phishing attempts

- Monitor accounts for unauthorized charges

- Understand the difference between debit and credit

- Question unfamiliar transactions

These skills transfer to adult financial security practices. Early exposure to account monitoring builds habits that protect against fraud and identity theft throughout life.

Integration with Broader Financial Education

A prepaid card works best as part of a comprehensive approach to money skills. The card handles practical transactions, but children also need concepts like budgeting, earning, investing, and giving.

Schools that teach life skills recognize that financial literacy requires multiple reinforcing experiences. Classroom instruction provides frameworks while hands-on practice through tools like prepaid cards makes concepts tangible.

Connecting Earning to Learning

The most powerful financial lessons often come through earning money rather than just receiving it. When children connect effort to income, they understand value differently than with simple allowances.

Some families tie card funding to completed chores or academic achievements. This creates a direct link between work and reward. The greenlight prepaid card can facilitate this through its chore tracking features, though the execution still depends on consistent family follow-through.

A life skills curriculum that includes financial education helps young people understand where money comes from, how to manage it responsibly, and how financial decisions impact future opportunities. Prepaid cards serve as tools within this larger educational framework.

Real-World Usage Scenarios

The greenlight prepaid card performs differently across various situations. Understanding these scenarios helps families set realistic expectations.

Daily School and Social Spending

For lunch money, school supplies, or outings with friends, the card works smoothly. Children can make purchases independently while parents see exactly where money goes. This visibility often surprises families who discover unexpected spending patterns.

A middle schooler buying lunch might quickly spend $50 per week on cafeteria food and snacks. This concrete data prompts discussions about packing lunch versus buying, or choosing healthier, less expensive options.

Online Shopping and Subscriptions

The card works for online purchases, which makes it useful as children get older and want to buy items themselves. Parents can approve or decline categories like online shopping, preventing surprise purchases.

However, subscription management can be tricky. Children may sign up for free trials that convert to paid subscriptions. The card's spending alerts help catch these conversions quickly, creating teaching moments about reading terms and canceling unwanted services.

Travel and Emergency Situations

The greenlight prepaid card provides security for children traveling to camps, school trips, or visiting relatives. Parents can instantly add funds if needed and monitor spending from a distance.

For emergencies, having a card means a child stranded somewhere can purchase food, transportation, or other necessities while parents coordinate solutions. This safety feature alone justifies the service for some families.

Age-Appropriate Implementation Strategies

Different ages require different approaches to using a prepaid card effectively.

Elementary school children (ages 6-10) benefit from simple allowances with clear rules. Parents might load a weekly amount and help the child track spending. At this age, the card mainly teaches that money is finite and purchases have trade-offs.

Middle school learners (ages 11-13) can handle category budgets and savings goals. They're ready to compare prices, make independent decisions within limits, and experience the consequences of poor choices in a low-risk environment.

High school teens (ages 14-18) should receive increasing autonomy. Parents might shift from rigid category controls to overall spending limits, preparing teens for college or independent living where they'll manage money without daily oversight.

Bold.org's review emphasizes tailoring features to developmental stages. A tool that micromanages a 17-year-old may prevent rather than promote financial maturity.

Customer Experience and Support Quality

User reviews on Sitejabber reveal mixed experiences with customer service. Many families report smooth operation with no need for support. When issues arise, however, response times and resolution effectiveness vary significantly.

Common support needs include:

- Activating new cards or troubleshooting activation failures

- Resolving disputed transactions

- Recovering locked or frozen accounts

- Canceling subscriptions or requesting refunds

- Technical problems with the mobile app

The company primarily offers email and chat support rather than phone assistance. Some parents prefer speaking directly with representatives, particularly for urgent issues affecting their child's access to funds.

Partnership Models and Institutional Access

Some financial institutions partner with Greenlight to offer the service to their customers. These partnerships may include discounted rates or integrated features with existing accounts.

Schools and youth organizations sometimes explore prepaid card programs for teaching financial literacy. The greenlight prepaid card can work in educational settings, though institutional adoption raises questions about equitable access and data privacy in school environments.

Alternative platforms designed specifically for educational use may better serve institutional needs. These specialized tools often include curriculum integration, classroom management features, and enhanced privacy protections appropriate for school use.

Making an Informed Decision for Your Family

Choosing whether to use the greenlight prepaid card depends on your specific situation. Consider these factors:

Budget: Can you comfortably afford $6-15 monthly for a financial education tool? Compare this cost to other enrichment expenses like music lessons or sports.

Technical comfort: Are you willing to manage finances through a smartphone app? Do you have reliable internet access?

Educational philosophy: Do you prefer hands-on learning tools or more traditional approaches to teaching money skills?

Child's age and maturity: Is your child ready for the responsibility of managing a card, even with parental oversight?

Alternatives: Have you explored no-fee options or traditional bank accounts that might meet your needs?

The greenlight prepaid card offers genuine value for families who will actively use its features. Simply giving a child a card without discussion, goal-setting, and regular review wastes the educational potential. The tool matters less than how you use it to create learning opportunities.

Parents seeking structured financial education should consider how a prepaid card fits within a broader strategy. Combining practical tools with formal instruction, regular family discussions about money, and real earning opportunities creates the strongest foundation for lifelong financial capability.

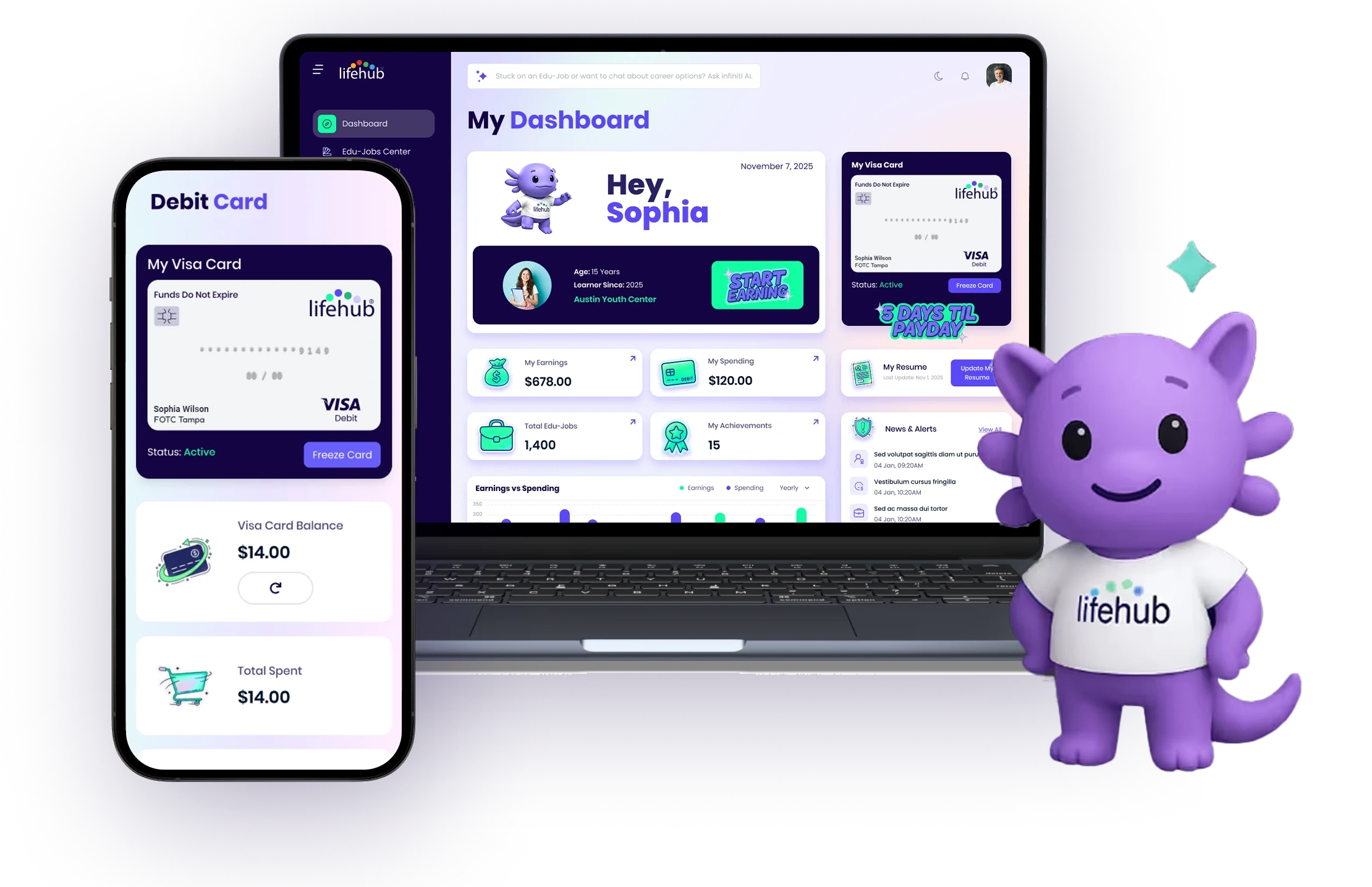

Teaching money skills requires more than tools. It demands consistent practice, meaningful conversations, and connections between effort and reward. The greenlight prepaid card can support this learning, but families have many options for building financial capability. Life Hub takes a different approach by combining financial education with real earning opportunities through Edu Jobs that teach money management, career skills, and academic content while depositing actual earnings to a debit card. This creates direct links between learning, effort, and financial reward that prepare young people for real-world success.

.avif)

.png)

.svg)

.svg)