Getting a debit card for a minor can feel like a big step for both parents and children. It's a tool that introduces real-world money management while keeping spending under control. In 2026, options for teen banking have expanded beyond traditional bank accounts, offering features like spending alerts, task-based earning, and financial education built right into the card experience. The key is finding an approach that matches your family's values and your child's readiness.

Understanding Age Requirements for Minor Debit Cards

Most traditional banks require account holders to be 18 years old to open a solo checking account with a debit card. However, legal age requirements for debit cards allow minors to access banking services through several alternative pathways. The most common option involves a joint account where a parent or guardian shares ownership and oversight.

Teen-focused accounts typically accept applicants as young as 13, though some programs start at age 6 or 8. Each financial institution sets its own minimum age based on the account type and features offered.

Joint Accounts vs. Teen-Only Options

Joint accounts give parents full visibility and control over their child's spending. Both the adult and minor can access the account, make deposits, and review transactions. The parent retains the ability to set spending limits, approve transactions, or freeze the card if needed.

Teen-only accounts offer more independence but still include parental oversight through a companion app. These accounts may have lower balance limits and restricted features compared to adult accounts. The minor holds primary ownership while parents monitor activity from their own device.

Types of Debit Cards Available for Minors

The market for youth banking has grown significantly. Each card type serves different needs and family preferences.

Traditional Bank Teen Accounts

- Offered by major banks and credit unions

- Usually free or low monthly fees

- ATM access through the bank's network

- Mobile app with basic budgeting tools

- May require minimum balance

Prepaid Debit Cards

- No bank account needed

- Load money as needed

- Can't overspend beyond loaded amount

- May have reload fees

- Limited fraud protection compared to bank cards

App-Based Teen Debit Cards

- Designed specifically for young users

- Strong parental controls built in

- Often include financial education content

- Instant spending notifications

- Digital-first experience with physical card option

Earning-Linked Debit Cards

- Connected to chore or task completion

- Automatic payment for completed activities

- Built-in incentive structure

- Combines earning with spending management

- May include educational components

Research from studies on household consumption and debit card usage suggests that having access to a debit card may influence spending habits. This makes the educational component critical when introducing a debit card for a minor.

Key Features to Look For

When choosing a debit card for a minor, specific features can make the difference between a learning tool and just another payment method.

| Feature |

Why It Matters |

Questions to Ask |

| Spending limits |

Prevents overspending |

Can you set daily/weekly limits? |

| Real-time alerts |

Keeps everyone informed |

Do both parent and teen get notifications? |

| Savings goals |

Builds planning skills |

Can multiple goals be tracked? |

| Transaction blocking |

Controls where card works |

Can you block certain merchant types? |

| Financial education |

Reinforces learning |

Is content age-appropriate? |

Parental controls should be comprehensive but not overwhelming. Look for the ability to pause the card instantly, approve transactions over a certain amount, and receive alerts for every purchase.

Fee structure varies widely across providers. Common fees include monthly maintenance, ATM withdrawals outside the network, card replacement, and international transactions. Some cards waive fees entirely for teen accounts.

Educational resources separate basic cards from those designed to build financial literacy. The best options integrate learning directly into the spending experience, helping young people understand concepts like youth financial education through practical application.

Teaching Money Management Through Card Usage

Simply handing a debit card to a minor won't automatically create good financial habits. Research shows parents have the strongest influence on their children's money behaviors, making active participation essential.

Setting Up Success From Day One

Start with clear expectations about what the card is for. Will it cover all spending money, or just specific categories like entertainment? Does your child need to contribute to savings before spending?

Have regular money conversations. Review transactions together weekly at first, discussing decisions made and alternatives considered. This turns abstract concepts into concrete examples your child can understand.

Connect spending to earning. When money comes from completed tasks or jobs, learners see the direct relationship between work and reward. This connection makes spending decisions more thoughtful because the money represents actual effort.

Common Scenarios and How to Handle Them

Lost or stolen card: Use this as a teaching moment about security. Show your child how to freeze the card immediately through the app, then report it and request a replacement. Discuss prevention strategies like never sharing the PIN.

Declined transaction: Instead of immediately adding funds, ask what happened. Was the balance too low? Did they forget about a previous purchase? Help them trace where the money went and plan better for next time.

Impulse purchase regret: Don't rush to fix it. Let them sit with the consequences of having less money for something they wanted more. These experiences build decision-making skills better than lectures ever could.

Security and Fraud Protection

Protecting a debit card for a minor requires attention from both parent and child. According to research on card fraud detection, understanding how fraud occurs helps victims respond more effectively.

Basic security practices include:

- Never sharing the card number or PIN with friends

- Using secure networks for online purchases

- Checking transactions regularly for unfamiliar charges

- Setting up alerts for all purchases

- Keeping the physical card in a safe place

Most bank-issued debit cards include zero-liability protection for unauthorized purchases. Prepaid cards may offer less protection, so read the terms carefully.

Teach your child to recognize common scams. Phishing texts claiming the card is locked, calls requesting account information, and fake merchant websites all target young, less-experienced users.

Comparing Debit Cards to Other Payment Methods

Parents often wonder whether a debit card for a minor is better than cash or other alternatives. Each method teaches different lessons.

Cash vs. Debit Card

Cash makes spending visible and finite. When the wallet is empty, spending stops. This tangibility helps younger children grasp money concepts.

Debit cards teach digital money management, which matters more as our economy moves toward cashless transactions. Research indicates that debit cards may decrease cash demand in households, reflecting broader payment trends.

The best approach often combines both. Use cash for younger children and transition to cards as they demonstrate readiness for digital money management.

Allowance Apps vs. Traditional Banking

Allowance apps let parents transfer money for chores or tasks without needing a bank account. These work well for younger children not ready for a full banking relationship.

Traditional teen banking offers more features, including ATM access, direct deposit capability, and check deposits. As teens take on part-time jobs, these features become more valuable.

Hybrid solutions like earning-based platforms combine task completion with real banking services, bridging the gap between simple allowance tracking and full financial independence.

Age-Appropriate Financial Concepts

Different ages require different approaches to money education. The debit card for a minor should match their developmental stage.

Ages 6-9:

- Understanding that money is earned, not infinite

- Difference between needs and wants

- Saving for short-term goals

- Basic addition and subtraction with money

Ages 10-13:

- Budgeting a fixed amount across categories

- Comparing prices before buying

- Understanding sales tax and fees

- Setting and tracking savings goals

Ages 14-17:

- Managing irregular income from jobs

- Planning for larger purchases over time

- Understanding how interest works

- Beginning to think about credit scores and future financial needs

Visual tools help learners grasp these concepts more effectively. Studies on data visualization in financial education show that seeing spending patterns, savings growth, and budget allocation improves comprehension across age groups.

Practical Setup Steps

Getting started with a debit card for a minor takes a few simple steps, though exact requirements vary by provider.

- Research options based on your child's age, your desired features, and fee structure

- Gather required documents like Social Security numbers, proof of address, and identification for both parent and child

- Open the account either online, in-branch, or through a mobile app

- Order the physical card if not provided immediately (digital cards often activate first)

- Set up parental controls including spending limits, merchant restrictions, and notification preferences

- Fund the account through transfer, direct deposit, or cash deposit

- Activate the card following the provider's instructions

- Review features together with your child before first use

Most accounts activate within a few days. Digital cards may be available immediately for online purchases while the physical card ships.

Connecting Cards to Learning Opportunities

The most effective debit card for a minor connects spending to broader skill development. When earnings come from completed learning activities, every dollar represents knowledge gained and skills practiced.

Platforms that integrate 21st century learning skills with financial capability create stronger outcomes. Learners see immediate results from their efforts while building academic knowledge, digital literacy, and practical abilities.

This approach shifts the conversation from "Can I have money?" to "What can I do to earn?" It builds agency, work ethic, and the understanding that financial resources connect directly to contribution and effort.

Beyond Basic Transactions

Look for opportunities to extend lessons beyond simple buying and spending. Discuss merchant categories, why certain stores charge more, how online vs. in-person shopping affects budgets, and what happens when account balances run low.

Use card statements as teaching tools. Review together monthly, identifying patterns, discussing surprises, and planning improvements. This regular practice builds financial awareness that will serve them throughout life.

When to Start and When to Wait

Not every child is ready for a debit card at the same age. Consider these readiness indicators instead of focusing solely on age.

Signs of readiness:

- Can explain where money comes from

- Demonstrates self-control with small amounts of cash

- Asks questions about prices and value

- Shows interest in saving toward goals

- Can handle disappointment when they can't buy something wanted

Reasons to wait:

- Frequently loses important items

- Shows no interest in money or doesn't ask questions

- Can't remember simple tasks or responsibilities

- Hasn't demonstrated basic math skills

- Reacts with tantrums to not getting what they want

Remember that how old you need to be for a debit card matters less than developmental readiness. Some eight-year-olds handle money responsibly while some fifteen-year-olds still struggle.

You can always start with limited features and expand access as skills grow. Begin with a small weekly amount, limited merchant types, and close supervision. Gradually increase freedom as competence increases.

Common Concerns Parents Have

"Won't a card make spending too easy?"

This depends on how you frame it. When cards connect to finite resources that must be earned, they can actually make spending more conscious than cash. The key is maintaining that clear connection between earning and spending.

"What if they lose it?"

Modern cards can be frozen instantly through an app. Replacements typically arrive within days. This inconvenience often teaches responsibility better than lectures about being careful.

"Will they overspend?"

Not if you set appropriate limits. Unlike credit cards, debit cards for minors only allow spending up to the available balance. Overdraft protection can be disabled entirely on teen accounts.

"Is this too much too soon?"

Start where your child is. A six-year-old doesn't need the same features as a sixteen-year-old with a part-time job. Choose a solution that can grow with them.

Making the Most of Teen Banking Features

Modern debit cards for minors include features that weren't available just a few years ago. Understanding what's possible helps you choose wisely and use the card effectively.

Instant notifications mean both you and your child see every transaction immediately. This creates natural conversation opportunities and catches mistakes or concerning purchases right away.

Spending categorization shows where money goes automatically. Seeing that half their balance went to food or gaming helps them understand patterns without manual tracking.

Savings automation lets you set up automatic transfers to savings goals. Paying yourself first becomes a habit rather than an afterthought.

Card controls let you turn specific features on or off. International transactions, online shopping, ATM withdrawals, and contactless payments can each be enabled or disabled based on current needs and trust level.

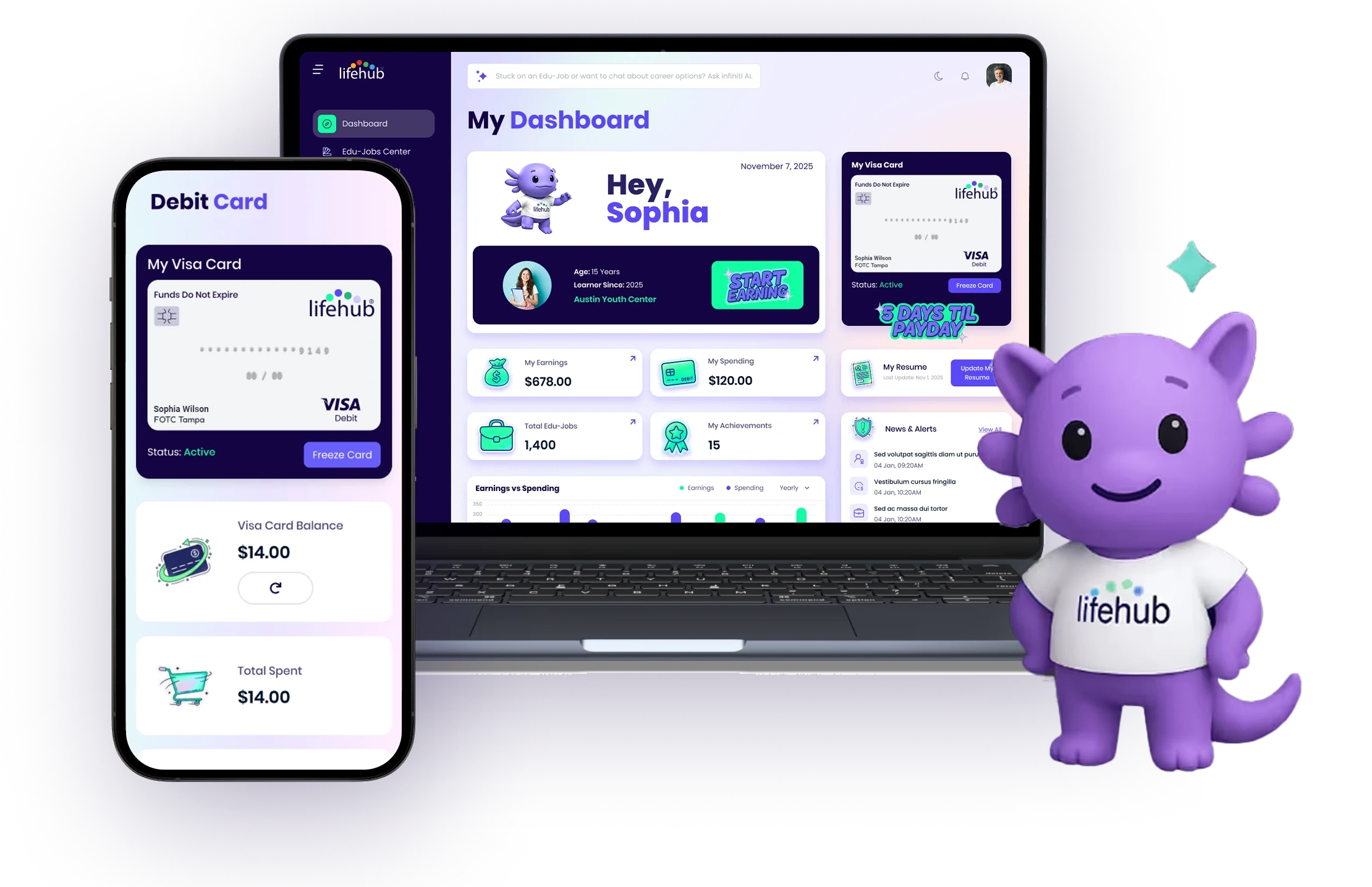

A debit card for a minor can be a powerful tool for building financial capability when paired with active guidance and clear expectations. By choosing an option that aligns with your values and your child's readiness, you create opportunities for practical learning that extends far beyond simple transactions. Life Hub connects earning to learning through Edu Jobs that build money skills, academic knowledge, and real-world capabilities, with earnings deposited directly to a Visa debit card that turns every dollar into a lesson in financial responsibility.

.avif)

.png)

.svg)

.svg)