Related Content

No items found.

In a rapidly evolving financial landscape, the importance of equipping the younger generation with robust financial literacy skills cannot be overstated. As digital transactions become the norm and financial products grow increasingly complex, young people often face economic decisions that could impact their future financial stability. This necessity has spurred a surge in youth financial literacy programs, which aim to empower young individuals with essential money management skills.

Imagine a world where teenagers not only understand how to balance a checkbook but also grasp the intricacies of student loans, credit scores, and investing. Empowering youth with these skills diminishes financial stress and lays a foundation for informed decision-making. Programs focusing on financial literacy are paving the way toward this ideal. These initiatives range from school-based curricula to community workshops, reaching a wide demographic across different socio-economic backgrounds.

For instance, the non-profit organization Junior Achievement provides programs that engage students with practical financial knowledge. According to Junior Achievement's official site, their "JA Finance Park" immerses students in a real-world simulation where they must manage budgets for necessities such as groceries, utilities, and transportation. This hands-on experience is invaluable, as it provides a safe space for students to learn from their mistakes without facing actual financial repercussions.

Furthermore, studies indicate that early exposure to financial education significantly reduces future financial mismanagement. According to research published by the Consumer Financial Protection Bureau, young adults who participated in financial literacy programs in high school reported higher credit scores and lower debt delinquency rates. These statistics underscore the long-term benefits and critical role of early financial education in shaping financially capable individuals.

For those interested in further exploring how modern learning approaches support financial literacy, insights are available through resources like the 21st Century Learning Skills which highlight complementary educational strategies.

As the dialogue around financial literacy gains momentum, it's vital to recognize the transformative power these programs hold for future generations. Through access to structured and engaging educational opportunities, today's youth are poised to become economically savvy adults who can adeptly navigate the complex financial terrains of tomorrow.

To fully appreciate the role of youth financial literacy programs, it's essential to understand why early financial education is critical. Introducing financial concepts at a young age lays the groundwork for responsible money management in adulthood. Young individuals who comprehend the basics of budgeting, saving, and investing develop skills that equip them to manage their finances effectively later in life.

These programs are designed to provide practical, actionable skills. For instance, high school students might engage in hands-on activities that simulate real-world financial situations. Programs like the Jump$tart Coalition for Personal Financial Literacy offer curricula that teach students to prepare budgets, calculate interest, and understand credit scores. Such experiences ensure that participants are not just theoretically knowledgeable but are adept at applying their knowledge practically [source].

Beyond practical skills, youth financial literacy programs aim to nurture positive financial behaviors. By learning about the pitfalls of debt and the benefits of saving, young people are more inclined to set financial goals and develop thriftiness. According to the Council for Economic Education, students who undergo financial education are more likely to save money, have checking and savings accounts, and invest in stocks [source]. This tangible shift in behavior underscores the efficacy of these programs in transforming financial attitudes.

A standout example of real-world application is the integration of digital platforms like smartphone apps and online courses. These tools offer immediate access to financial information, allowing youth to learn at their own pace. Furthermore, many of these programs are supported by nonprofits and educational institutions, ensuring affordability and accessibility. A noteworthy mention is "Moneythink," an organization leveraging technology to provide mentorship and customized financial lessons directly to students’ smartphones. For more insights into technological advancements in education, the blog AI Education For Kids explores similar innovations.

Incorporating technology not only modernizes financial literacy programs but also aligns them with the digital preferences of today’s youth. By harnessing these tools, educators can engage students more dynamically, making the learning process interactive and effective.

Addressing financial literacy in today's youth is crucial for fostering responsible future adults capable of making informed economic decisions. These programs play an essential role in shaping the financial habits of young individuals. By offering practical knowledge and real-world applications, they empower students to understand and navigate complex financial landscapes. For example, children who learn about budgeting, saving, and investing early on are more likely to avoid debt and manage their finances effectively in adulthood. According to the National Endowment for Financial Education, students participating in financial literacy courses have shown an improvement of up to 15 percentage points in credit scores within two years.

One standout example is the adoption of interactive tools and games to engage students in learning about money management. Gamified learning experiences are particularly effective in keeping the attention of young minds. Programs like Junior Achievement's Finance Park use simulations to educate students on personal finance by allowing them to make decisions about expenses involving a set budget. In these controlled environments, students encounter real-life scenarios that compel them to prioritize needs over wants.

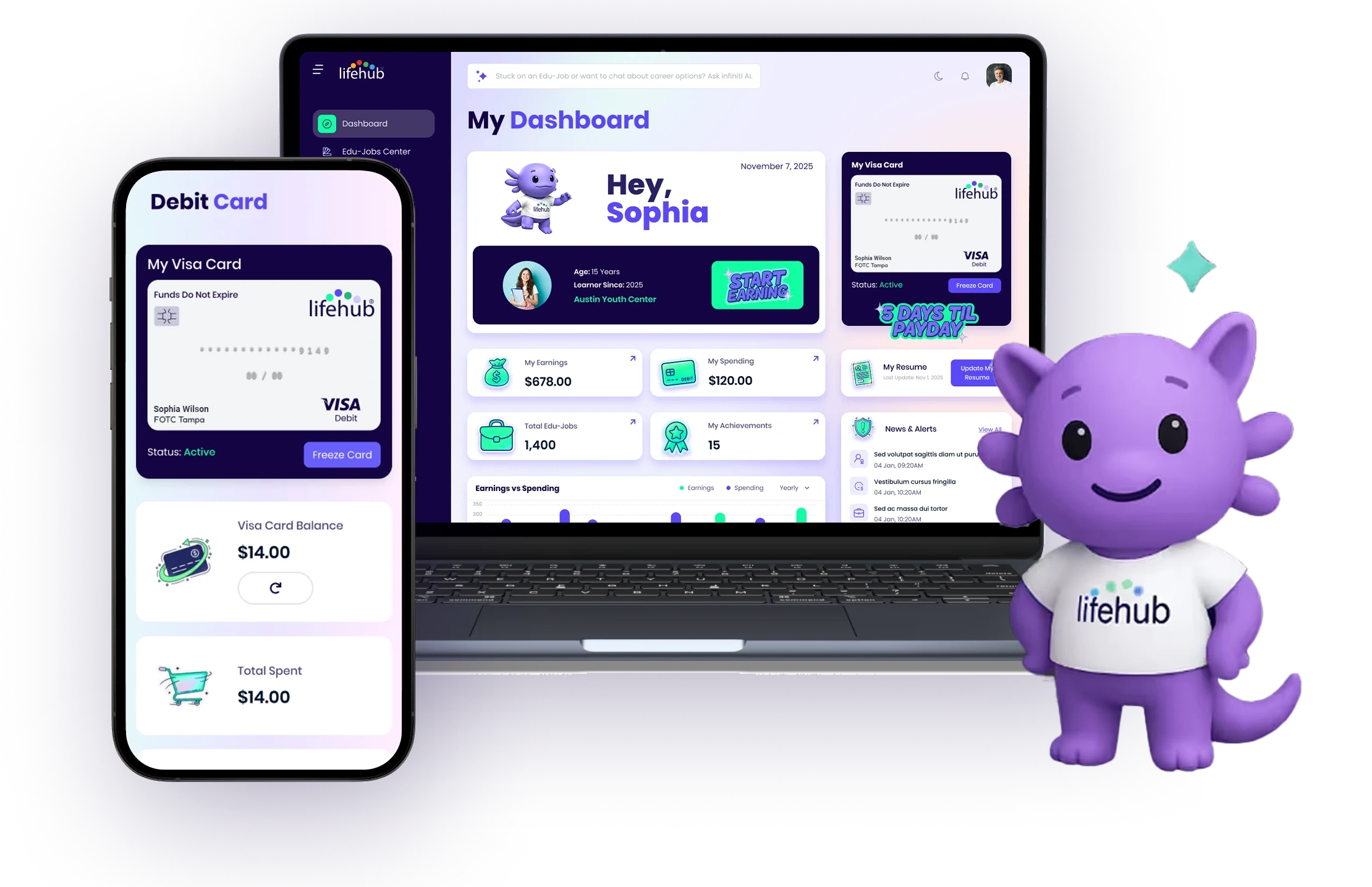

Moreover, it's essential to recognize the critical role of technology in enhancing the reach and effectiveness of youth financial literacy programs. Online platforms such as Life Hub offer comprehensive resources tailored to the needs of young learners, facilitating an engaging and interactive approach to financial education. These platforms embed financial literacy within accessible and relatable contexts, further encouraging consistent participation.

Community-based initiatives also provide invaluable support in spreading financial literacy among youths. Schools partnering with financial institutions to create workshops and seminars have proven successful. These initiatives offer students real-world exposure by inviting financial experts to discuss practical money management skills. Such community efforts help demystify complex financial concepts, thus preparing young adults for the economic aspects of life.

Expanding the outreach of financial literacy programs is not just beneficial but crucial for today’s fast-paced economic environment. As we move toward a more technology-driven world, it's vital for educators to leverage available resources effectively. To explore the broader implications of integrating technology in education, readers can access insights on Youth Oriented Organizations provided by Life Hub, detailing innovative ways in which AI is shaping financial literacy.

Building on the foundations addressed earlier, successful youth financial literacy programs hinge on thoughtful design and evidence-based delivery. For instance, a meta‑analysis of U.S. high school programs involving approximately 12,000 students found that these initiatives significantly improve both financial knowledge (Hedges’ g = 0.45) and financial behaviors (Hedges’ g = 0.35), demonstrating measurable gains when programs are well‑constructed and integrated into educational settings Yeboah (2024).

It’s essential to note that compulsory, school‑based instruction tends to produce stronger results than optional after‑school offerings. Research from the Inter‑American Development Bank highlights that mandatory coursework yields large, robust improvements in financial literacy, while voluntary programs often deliver modest outcomes IDB working paper. Embedding financial literacy into the standard curriculum ensures equitable access and consistent engagement.

Programs leveraging interactive methods—such as simulations, games, and real‑life exercises—tend to foster deeper comprehension and retention. A study published in Frontiers in Education demonstrates that initiatives utilizing digital platforms, workshops, and simulations boost engagement and reinforce financial behavior more effectively than lecture‑based models Frontiers (2024). Incorporating such tools encourages active participation and practical application of financial principles.

Behaviorally informed approaches can especially benefit youth with limited prior exposure to financial education. An experimental trial involving a mobile app paired with biweekly monitoring produced substantial literacy gains and heightened financial awareness, particularly among participants with lower baseline knowledge Frisancho et al. (2023). This suggests that tailored, technology‑assisted programs can be powerful instruments for bridging educational gaps.

Beyond knowledge gains, the true measure of impact lies in behavioral shifts and sustained financial wellbeing. Some models, like the Boston Youth Credit Building Initiative, use randomized controlled trials and track credit scores and behaviors before and after participation. These rigorous evaluations have demonstrated favorable impacts on money management skills and responsible financial practices Modestino et al. (2019). Capturing such data enables educators and policymakers to refine and optimize program design.

Collectively, these insights underscore the importance of structured, engaging, and evidence‑driven youth financial literacy programs. By weaving mandatory instruction with interactive learning, digital access, and long-term evaluation, educators can significantly elevate both understanding and real-world financial behavior.

As we reflect on the impact of youth financial literacy programs, it's clear that they are pivotal in equipping the younger generation with essential financial skills. These programs provide a foundational understanding of money management, budgeting, and saving, thereby empowering youths to make informed decisions that will benefit them throughout their lives.

One actionable insight is the importance of incorporating financial education early in childhood. Schools and community organizations should consider integrating interactive and engaging financial tools, like board games and digital apps, to make learning both effective and enjoyable. Real-life applications, such as setting up a savings account or planning a small budgeting project, encourage practical understanding and retention of financial concepts.

Moreover, partnerships between educational institutions and financial organizations can enhance the reach and effectiveness of these programs. Such collaborations can provide students with access to workshops and seminars conducted by financial experts, adding valuable real-world perspectives. According to the National Endowment for Financial Education, students who participate in financial literacy programs are more likely to develop positive financial habits.

To solidify these skills, parents also play a vital role by modeling responsible financial behavior at home. Engaging children in discussions about family budgeting, or even involving them in household financial decisions where appropriate, can reinforce what they learn in formal programs. This integration of home and classroom education maximizes the potential for a lifelong impact.

For those eager to explore comprehensive solutions, Life Hub offers a holistic platform that combines educational resources with tailored learning experiences. This offers a robust pathway to support parents and educators in nurturing financially literate youths.

In conclusion, youth financial literacy programs are not just an educational tool but a necessary investment in our future. By harnessing engaging teaching strategies, fostering partnerships, and involving families, we ensure that the new generation not only understands the value of money but also how to use it wisely. As these programs continue to evolve, they will undoubtedly remain a critical component of our educational landscape.

Whether you're parents, or a homeschool family, Life Hub is your partner to help you

raise super strong kids.

Turning high value micro-learning into real-world cash and non-cash rewards with tokenization.

.svg)

Electus Global Education Co, Inc. has received support from The American Heart Association Social Impact Funds.

.svg)