When you decide to help a young person build money skills, getting them a debit card can be a powerful first step. The ability to minor debit card apply online has made this process simpler than ever. Parents and guardians can now set up banking tools from home without visiting a branch. This guide walks through everything you need to know about applying for a minor debit card online in 2026, from age requirements to choosing the right card program.

Understanding Minor Debit Cards

A minor debit card functions like a standard debit card but comes with parental oversight features. These cards connect to a checking or savings account designed specifically for young people under 18. Unlike prepaid cards, debit cards for minors typically link to a real bank account.

Most programs allow parents to monitor transactions in real time. You can set spending limits, block certain merchant categories, and receive alerts when your child makes a purchase. Youth financial education becomes hands-on when young people can practice real transactions with real consequences.

Age Requirements Vary by Provider

Different banks and financial programs set different minimum ages. Some cards are available for children as young as 6, while others require teens to be 13 or older. A few institutions may require minors to be at least 16 before they can hold a card linked to their own account.

When you research options to minor debit card apply online, check the specific age threshold for each program. Some providers, like HDFC Bank, offer different account types based on age brackets, with self-operated accounts available for children over 10 years old.

What You Need Before You Apply

The online application process requires specific information and documents. Gathering these materials beforehand makes the process faster and reduces the chance of delays.

Parent or Guardian Information:

- Full legal name and Social Security number

- Date of birth and contact information

- Valid government-issued ID (driver's license or passport)

- Proof of address (utility bill or lease agreement)

Minor's Information:

- Full legal name and Social Security number

- Date of birth

- Contact information (email or phone for older teens)

Some banks may ask for additional verification. Setting up a debit card for a minor typically requires the parent to already have an account with the institution or to open one simultaneously.

Joint vs. Custodial Accounts

Understanding account types helps you make the right choice. A joint account means both parent and child have equal access and ownership. A custodial account means the parent controls the account until the child reaches the age of majority (18 or 21, depending on the state).

| Account Type |

Control |

Access |

Legal Ownership |

| Joint |

Shared |

Both parties can transact |

Both parties |

| Custodial |

Parent until age of majority |

Parent approves transactions |

Child (parent manages) |

| Teen Checking |

Parent oversight |

Teen primary user |

Typically joint |

Most programs designed for minors use a hybrid approach. The minor gets their own card and login, but the parent retains oversight through a separate parent account or app.

Step-by-Step Online Application Process

When you're ready to minor debit card apply online, the actual process takes about 10 to 15 minutes if you have all your documents ready. Here's how it typically works.

Choose Your Provider

Research which banks or financial technology companies offer minor debit cards. Compare features like fees, parental controls, and educational tools to find the best fit for your family. Some traditional banks offer these accounts, while newer fintech companies specialize in teen banking.

Look for programs that emphasize financial literacy. Cards that integrate with educational platforms help young people learn while they spend. Programs that reward learning activities create positive associations with money management.

Start the Application

Visit the provider's website and locate the application for minor or teen accounts. You'll create an account using your email address and set up a password. The system will ask you to verify your email before proceeding.

Application Steps:

- Enter parent or guardian information

- Provide minor's personal details

- Upload or enter identification documents

- Link funding source (bank account or card)

- Review terms and conditions

- Submit application

Most providers run a soft credit check on the parent, which won't affect your credit score. Understanding the rules and requirements before applying helps you prepare the right information.

Wait for Approval

Approval can be instant or may take a few business days. Instant approvals happen when the system can verify all information electronically. Manual reviews occur if there are discrepancies or if additional verification is needed.

You'll receive an email notification about your application status. If approved, the physical card typically arrives within 7 to 10 business days. Many providers now offer virtual cards immediately, allowing your teen to start using the card for online purchases right away.

Setting Up Parental Controls

After approval, you'll want to configure the oversight features. These controls make the difference between a teaching tool and just another spending card. Most apps let you customize settings based on your family's values and your child's maturity level.

Spending Limits and Allowances

Set daily, weekly, or monthly spending caps. Some platforms let you set different limits for different transaction types (ATM withdrawals vs. online purchases). You can automate allowance deposits on a schedule, teaching your teen to budget within a regular income.

Control Options:

- Transaction amount limits

- Daily spending caps

- Category restrictions (no gambling, alcohol)

- Geographic limitations

- Time-based controls (school hours restrictions)

These features turn the card into a financial education tool. When teens bump up against a limit, they learn to prioritize purchases and plan ahead.

Monitoring and Notifications

Real-time alerts keep you informed without hovering. Set up notifications for every transaction or only for purchases over a certain amount. You can receive alerts via text, email, or push notification through the app.

Review transaction history together with your teen regularly. This creates natural opportunities to discuss wants versus needs, comparison shopping, and impulse control. Making these conversations routine builds money skills that last a lifetime.

Educational Features to Look For

The best minor debit card programs go beyond basic banking. They include tools and resources that actively teach financial concepts. When you minor debit card apply online, prioritize programs with robust educational components.

Built-In Learning Modules

Some cards integrate financial literacy lessons directly into their apps. These might include videos, quizzes, or interactive scenarios about budgeting, saving, and credit. Digital literacy and 21st-century learning skills become more relevant when young people can apply concepts immediately with their own money.

Look for platforms that explain financial terms in plain language. The best programs use age-appropriate examples that connect to a teen's actual life. Lessons about saving for a concert ticket resonate more than abstract discussions of compound interest.

Savings Goals and Tracking

Many apps let teens set savings goals with visual progress trackers. Seeing a progress bar fill up provides immediate feedback and motivation. Some programs match savings contributions or offer interest on balances, teaching the concept of earning money on money.

Educational Banking Features:

| Feature |

Educational Value |

Example |

| Savings goals |

Delayed gratification |

Save for new phone |

| Spending analytics |

Budget awareness |

Charts showing category spending |

| Transaction categorization |

Expense tracking |

Auto-labels food, entertainment |

| Earning opportunities |

Work-reward connection |

Chore payments, task completion |

Programs that connect learning directly to earning create powerful motivation. When young people can complete micro-learning tasks for real money, they see immediate results from their effort.

Common Mistakes to Avoid

Even when you carefully minor debit card apply online, certain pitfalls can reduce the educational value or cause frustration. Being aware of these common issues helps you set up the account for success.

Not Discussing Expectations First

Before handing over the card, have a clear conversation about rules and responsibilities. Discuss what the card can be used for, consequences for misuse, and what happens if the card is lost or stolen. Written agreements work well for some families.

Young people need to understand that debit cards use real money. Unlike credit cards, there's no grace period or billing cycle. The money leaves the account immediately. This reality makes debit cards excellent teaching tools but requires clear communication.

Overlooking Fees

Read the fee schedule carefully. Some minor accounts charge monthly maintenance fees, ATM fees, or transaction fees. Others are completely free. Understanding the requirements includes knowing all potential costs.

Common Fee Types:

- Monthly account maintenance

- ATM withdrawals (out of network)

- Replacement card fees

- Overdraft or insufficient funds

- Paper statement fees

- Inactivity fees

Choose a card with minimal fees, especially if your teen is just starting out. High fees can quickly drain a young person's limited funds and create negative associations with banking.

Setting and Forgetting

A minor debit card requires ongoing engagement. Check in regularly about spending patterns, discuss purchases, and adjust limits as your child demonstrates responsibility. The card is a tool for teaching, not a solution that works on autopilot.

Use the card as a conversation starter. When your teen makes a questionable purchase, resist the urge to lecture. Ask questions instead. "What made you decide to buy that? Are you happy with the purchase? What would you do differently next time?"

Security Considerations

Teaching young people about card security protects them now and builds habits that serve them as adults. When you minor debit card apply online, security features should factor into your decision.

Protecting Card Information

Explain that the card number, expiration date, and CVV code should never be shared except during legitimate purchases. Teach your teen to recognize phishing attempts and suspicious websites. Role-play scenarios where someone asks for card information inappropriately.

Most teen banking apps include card lock features. If the card is misplaced, your teen can instantly freeze it through the app. This prevents unauthorized transactions while you look for the card. If it's truly lost, you can order a replacement through the same app.

Fraud Protection

Legitimate banking programs include zero-liability fraud protection. This means your teen won't be responsible for unauthorized charges if the card is stolen and used. Report suspicious activity immediately through the app or customer service line.

Teach your teen to review transactions regularly, not just when checking their balance. Fraudulent charges can be small initially as criminals test whether a card is active. Catching these early prevents larger problems.

Alternative Approaches Worth Considering

While traditional bank cards remain popular, newer approaches combine banking with education in innovative ways. These alternatives can enhance or replace standard minor debit cards depending on your goals.

Earning-Based Debit Programs

Some programs connect card funding directly to learning activities or chore completion. Rather than receiving a free allowance, young people earn money by completing educational tasks or household responsibilities. This creates a direct link between effort and reward.

Digital platforms now make it possible to assign tasks, verify completion, and automatically deposit earnings. This approach teaches that money comes from work, not from parents simply transferring funds. The lesson becomes especially powerful when the tasks themselves build skills.

For families looking to help their teens build digital products or learn to monetize their skills, pairing a debit card with entrepreneurship education creates powerful opportunities. Young people can receive payments for real work, learning to manage income from multiple sources.

Hybrid Physical and Digital Cards

Some providers offer both physical cards and virtual cards that exist only in digital wallets. Virtual cards work with contactless payment systems on phones and smartwatches. This introduces teens to technology they'll use throughout their lives while maintaining parental oversight.

Virtual cards can be created instantly for specific purposes. Need to let your teen buy something online? Generate a virtual card with a specific spending limit that expires after one use. This provides security and control while teaching responsible online shopping.

When Teens Are Ready for More Independence

As young people mature and demonstrate responsibility, gradually reduce restrictions. This prepares them for the full independence of adult banking. The timeline varies for each individual based on their decision-making skills and financial literacy.

Transitioning to Full Access

Some minor debit card programs automatically convert to adult accounts when the cardholder turns 18. Others require opening a new account. Plan for this transition in advance. Discuss what changes when parental oversight ends and why continued good habits matter.

Before removing controls completely, try a trial period with expanded limits and reduced monitoring. If your teen maintains responsible behavior, they're probably ready for more freedom. If problems arise, you can step back and provide more structure.

Transition Checklist:

- Review credit score basics and how to build credit

- Discuss adult banking fees and how to avoid them

- Explain credit cards versus debit cards

- Cover emergency fund concepts

- Practice creating a budget without parental input

Building Toward Financial Independence

The goal of a minor debit card isn't just to provide spending money. It's to develop the skills and habits that lead to financial security as an adult. Personal development and financial capability go hand in hand when young people practice real-world money management.

Consider expanding beyond just spending. Introduce concepts like investing, credit scores, and tax basics as your teen approaches adulthood. Some platforms offer investment accounts for minors that work alongside the debit card.

Comparing Popular Programs

Multiple providers now offer the ability to minor debit card apply online. Each has different features, fees, and age requirements. Comparing options helps you find the right fit.

| Provider |

Minimum Age |

Monthly Fee |

Key Features |

Educational Tools |

| Chase First Banking |

6 |

$0 |

Parental controls, no overdraft fees |

Basic budgeting tools |

| Greenlight |

6+ |

$4.99-$14.98 |

Investing, chore tracking |

Financial literacy games |

| GoHenry |

6-18 |

$4.99 per child |

Task management, spending limits |

In-app money missions |

| Current |

13+ |

$0-$4.99 |

Teen-focused, instant notifications |

Savings pods |

| Capital One MONEY |

8+ |

$0 |

Linked to parent account |

Basic tracking |

Fee structures vary significantly. Some charge per child, while others offer family plans. Free accounts may have fewer features but work well for families on tight budgets. When deciding on the best debit card for kids, consider both cost and educational value.

Legal and Tax Considerations

Opening a bank account for a minor involves some legal and tax implications worth understanding. While not complicated, knowing these details prevents surprises.

Custodial Account Rules

Custodial accounts are governed by the Uniform Transfers to Minors Act (UTMA) or Uniform Gifts to Minors Act (UGMA), depending on your state. The minor technically owns the account, but the custodian (parent) manages it until the child reaches the age of majority.

Once your child reaches 18 (or 21 in some states), the account legally becomes theirs. You cannot restrict access or take back the funds. This matters for families with significant account balances. For typical spending accounts with modest balances, this rarely creates issues.

Tax Reporting

Interest earned on a minor's bank account may be taxable. For 2026, the first $1,300 of unearned income (interest, dividends) for a child under 18 is tax-free. The next $1,300 is taxed at the child's rate (usually low). Amounts above that are taxed at the parents' rate under the "kiddie tax" rules.

For typical teen spending accounts, interest earnings fall well below these thresholds. You'll receive a 1099-INT form if interest exceeds $10 in a year. Keep these forms for tax filing purposes, but most families won't owe tax on teen account interest.

Making the Most of the Card

Getting the card is just the beginning. Maximizing its educational value requires intentional use and regular conversation. Here are strategies that turn a piece of plastic into a powerful teaching tool.

Regular Money Conversations

Schedule monthly money talks to review spending, discuss goals, and adjust strategies. Make these conversations judgment-free zones where mistakes become learning opportunities. Ask questions that develop critical thinking rather than providing all the answers.

Talk about your own financial decisions. When you choose not to buy something or save for a specific goal, explain your thinking. Young people learn more from observing real behavior than from lectures about what they should do.

Connect Spending to Values

Help teens recognize that spending reflects priorities. When someone says something matters to them but never spends money or time on it, actions and words don't align. Reviewing spending patterns can reveal true priorities.

This awareness becomes especially valuable as teens grow into adults making bigger financial decisions. The person who learns at 14 that spending $50 monthly on gaming might mean sacrificing other goals will make better choices at 24 about car payments or student loans.

Celebrate Financial Wins

Recognize when your teen demonstrates good financial judgment. Reached a savings goal? Acknowledge the discipline that required. Comparison shopped and found a better price? Celebrate the critical thinking. Positive reinforcement builds habits.

Financial education shouldn't focus only on preventing mistakes. Highlighting successes creates positive associations with money management and builds confidence in financial decision-making.

Integration with Broader Financial Education

A debit card works best as part of a comprehensive approach to financial literacy. When teens learn concepts and immediately practice them with real money, knowledge sticks.

Connecting Learning to Earning

Programs that tie earnings to educational completion create powerful motivation. When a teen completes a module about budgeting and then receives payment deposited to their debit card, the lesson becomes concrete. The abstract concept of budgeting connects to the real experience of managing actual money.

This approach mirrors adult work life more accurately than allowances. Adults earn money by completing tasks and providing value, not by existing. Young people who learn this connection early develop stronger work ethics and better appreciate the relationship between effort and income.

Building Multiple Skills Simultaneously

Financial literacy intersects with numerous other capabilities. Managing a debit card requires digital literacy, decision-making, planning, and self-control. Tracking spending involves math and data analysis. Evaluating purchases requires critical thinking.

When you minor debit card apply online as part of a broader development strategy, you're building multiple competencies at once. The card becomes a tool for practicing skills that extend far beyond banking.

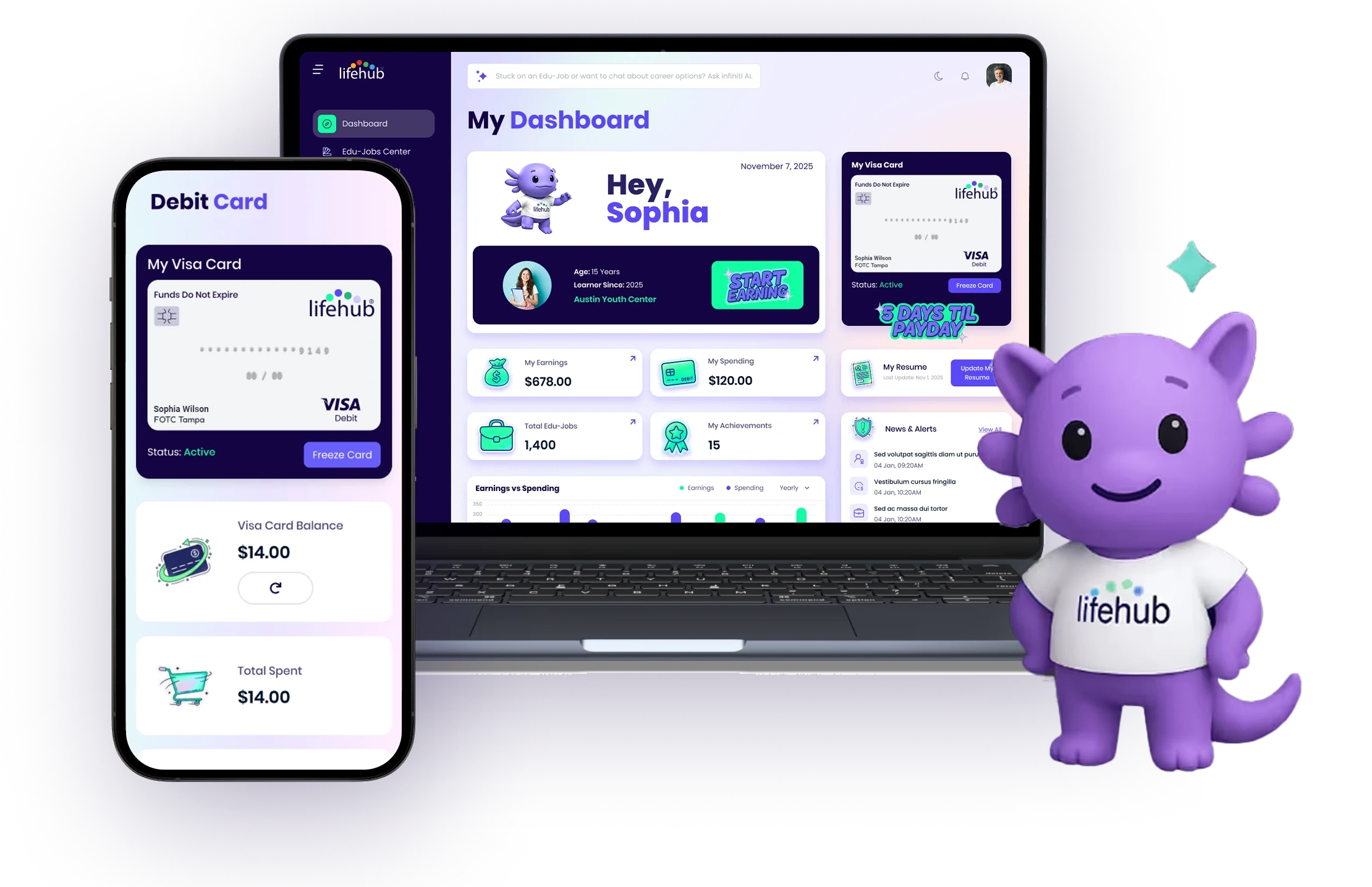

Getting a debit card for a minor through an online application gives young people hands-on experience with money management in a controlled environment. The combination of real spending power and parental oversight creates ideal conditions for developing financial capability. When you're ready to take financial education further, Life Hub connects learning directly to earning through paid educational tasks that deposit real money onto a Life Hub Visa debit card, turning every completed lesson into tangible progress toward both knowledge and financial independence.

.avif)

.png)

.svg)

.svg)