Related Content

No items found.

In today's rapidly evolving financial landscape, traditional retail deposit acquisition strategies are encountering unprecedented challenges. Demographic shifts, rising customer acquisition costs, and the swift spread of digital-native financial technologies are compelling financial institutions to innovate. With customer acquisition costs for mature consumers approaching $743, a radical re-evaluation is necessary. This article delves into the benefits of a downstream deposit acquisition strategy focused on early-life engagement, leveraging the Life Hub programmatic framework to cultivate lifelong depositors and enhance Community Reinvestment Act (CRA) impact.

Capturing customers early in life is becoming a cornerstone strategy for maximizing customer lifetime value. Establishing a primary banking relationship with minors is not merely a noble civic initiative; it's a strategic necessity. Empirical evidence underscores that engaging young consumers significantly boosts long-term retention. Approximately 45% of youth account holders remain loyal to their initial financial institution as adults, according to banking studies. This strong consumer inertia underscores the importance of acquiring customers early and nurturing their financial journey from minor to adult.

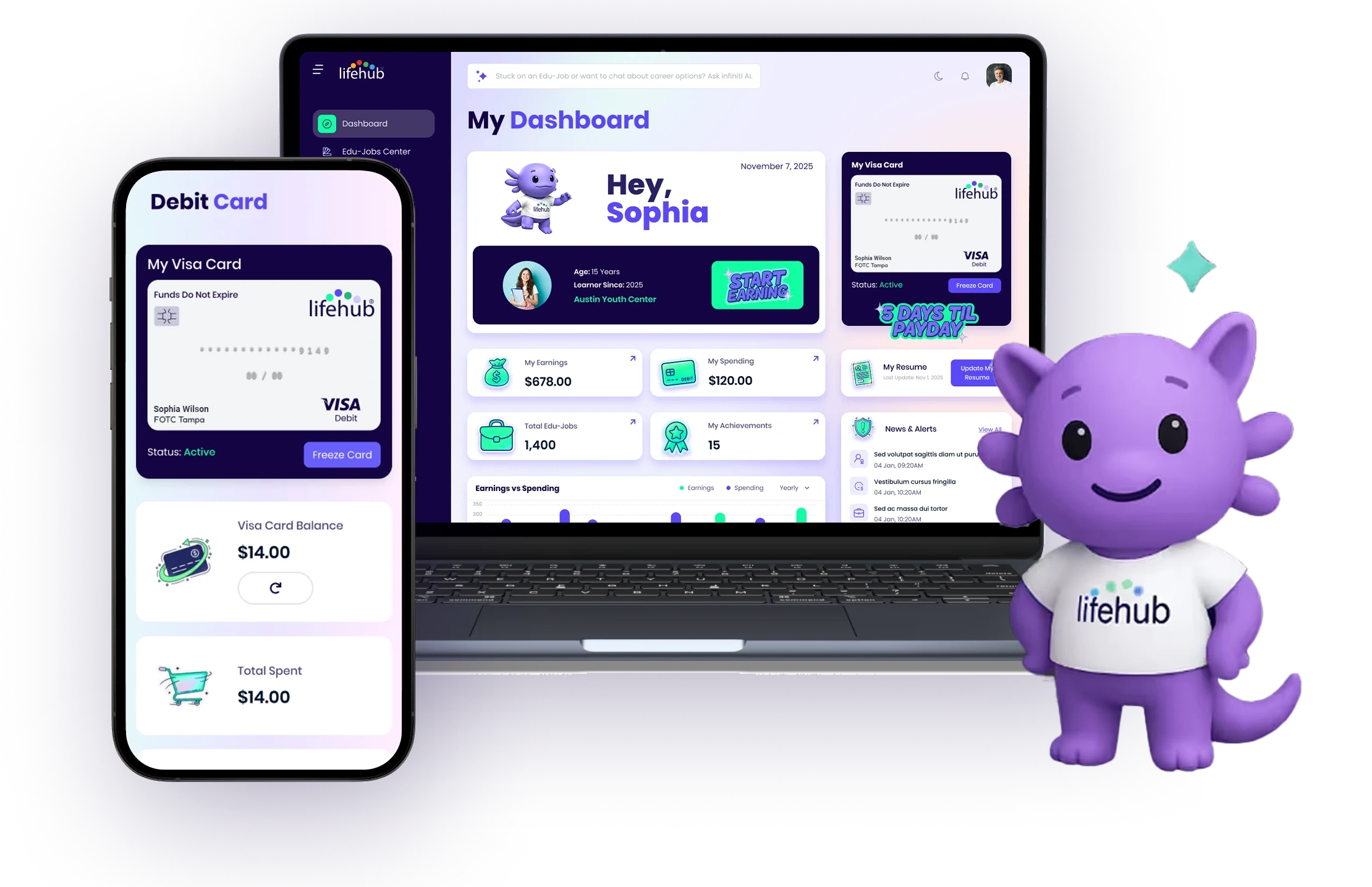

Electus Global Education Co’s Life Hub redefines youth financial engagement by transitioning from theoretical learning to an active, monetized model. Through Life Hub, young learners ages 6 to 18 complete micro-learning modules called "Edu-Jobs," earning real money that is deposited onto a secure Life Hub Visa Rewards Card. This innovative approach aligns closely with modern banking goals, ensuring that financial literacy is not only taught but actively practiced.

For financial institutions, this means not only capturing lifetime brand primacy but also constructing a resilient, low-cost deposit foundation. By targeting parents, who are the primary gatekeepers for youth financial products, banks and credit unions can tap into a 78% referral pipeline. This strategic method of early engagement is proving crucial in a world where 31% of teenagers use fintech alternatives like Cash App and Venmo.

For more on this strategic approach, explore insights on banks and credit unions adapting to modern financial education models.

The landscape of retail deposit acquisition is evolving rapidly, driven by demographic shifts, escalating customer acquisition costs, and the burgeoning influence of digital-native financial technologies. Traditional strategies are under pressure as the cost to acquire mature retail banking consumers approaches $743. This pressing economic backdrop forces institutions to rethink their approach to acquiring young depositors early in their financial journeys.

Securing a primary banking relationship with minors is key to maximizing long-term client relationships and sustaining balance sheet growth. Statistics reveal that 45% of minor account holders maintain their banking relationship into adulthood, highlighting the importance of early capture. Establishing these relationships sets the stage for a lifetime of financial engagement encompassing products like auto loans and mortgages.

Despite the potential, community banks and credit unions face significant threats from agile fintech firms. With 31% of teenagers using apps like Cash App and Venmo, traditional banks must innovate to retain relevance. A well-designed youth banking program with digital tools is imperative to counteract this trend.

Financial institutions can successfully navigate this changing terrain by implementing robust, digital-first youth banking suites. Engaging parents—who initiate 78% of minor accounts at their own banks—can significantly enhance acquisition efforts. By focusing on parental trust and convenience, banks can leverage this natural referral pipeline effectively.

Programs like the Life Hub emphasize financial literacy and early-life financial engagements through experiential education models. Transitioning from passive savings accounts to active, "learn-and-earn” programs not only engages young consumers but also aligns with regulatory demands like the Community Reinvestment Act. This dual approach of regulatory compliance and customer acquisition forms a strategic pillar for financial sustainability.

The rise of digital-native financial technologies presents both a challenge and an opportunity for traditional retail banking institutions. With the customer acquisition cost for mature banking consumers nearing $743, banks are compelled to innovate. One promising strategy involves engaging young depositors early in their financial journey. This approach not only builds a low-cost deposit foundation but also fosters lifelong customer relationships.

Traditional banks face unprecedented competition from fintech companies. 31% of teenagers currently use peer-to-peer payment apps like Cash App and Venmo, bypassing traditional banking options. However, banks can counter this trend by offering engaging, tech-savvy alternatives that appeal to youth. The Life Hub Programmatic Framework stands out in this regard, by combining financial literacy with interactive technology.

Life Hub employs a "learn-and-earn" model where students complete micro-learning modules called "Edu-Jobs." Each module affords learners real money, deposited onto a co-branded Life Hub Visa Rewards Card, aligning perfectly with the interests and digital habits of young users. Such initiatives are crucial in capturing and retaining young customers, ensuring that institutions remain their preferred financial partner into adulthood.

Incorporating parents into the financial education of their children offers a strategic advantage. Given that 78% of parents open their child's first debit account at their own financial institution, banks can leverage this by targeting parents with robust youth banking suites. Life Hub's turnkey parent dashboards and real-time transaction tracking deepen these relationships, promoting a multi-generational customer base.

For banks, aligning strategic initiatives with regulatory requirements like the Community Reinvestment Act (CRA) is crucial. Life Hub transforms CRA compliance budgets into customer acquisition opportunities by funding financial education initiatives targeted at low-to-moderate-income (LMI) youth. This model not only meets federal mandates but also introduces unbanked families to banking services, thus expanding the institution's customer base.

In conclusion, by integrating cutting-edge digital solutions like Life Hub, traditional banks can effectively cultivate lifelong depositors and enhance their Community Reinvestment Act impact. This holistic approach is not just a strategic necessity but a pathway to sustainable growth in today's competitive banking landscape.

As traditional retail deposit acquisition strategies face mounting challenges, the integration of innovative digital solutions like Life Hub offers a transformative approach. The strategy of engaging young consumers early through platforms that connect learning with real-world applications creates a robust foundation for lifelong banking relationships.

The Life Hub's "learn-and-earn" model fosters financial literacy in youths by providing rewards for completing educational modules. This hands-on learning incentivizes children to practice sound financial habits early, ultimately enhancing the lifetime value of customer relationships. Approximately 45% of youth account holders maintain their banking relationship into adulthood, underscoring the effectiveness of early engagement. For those interested in AI's role in education, AI Literacy Builds Futures provides further insights.

Community banks can harness Life Hub to convert Community Reinvestment Act (CRA) compliance expenses into proactive community-building initiatives. For example, partnerships like those with the YMCA of Metropolitan Chicago and Boys & Girls Clubs have shown success in deploying Life Hub to empower local youths. These programs not only fulfill CRA obligations but also establish positive community ties and create future banking customers.

Life Hub's platform features like co-branded portals and Visa debit cards allow financial institutions to stay relevant in the competitive landscape dominated by fintech alternatives. With over 31% of teenagers using peer-to-peer payment apps, banks must adapt by offering equivalent digital solutions. This approach ensures brand presence remains strong throughout the consumer’s financial journey.

Leveraging Life Hub’s Infiniti AI™ Analytics for real-time monitoring and compliance reporting provides significant advantages. Financial institutions gain access to audit-ready compliance data while simultaneously gathering customer insights to refine future strategies. This feature helps simplify regulatory examinations and supports robust CRA filings, transforming a potential cost center into an opportunity for growth.

Ultimately, embracing innovative tools such as Life Hub can ensure traditional banks cultivate sustainable growth by securing the next generation of depositors, thereby maximizing their Community Reinvestment Act impact.

In today's rapidly evolving financial landscape, traditional retail banks and credit unions face significant challenges. To address these, instituting a downstream deposit acquisition strategy has become paramount. This approach not only ensures sustainable growth but also aligns with socially responsible banking practices under the Community Reinvestment Act (CRA). The integration of early-life account acquisition within banking models, such as through Life Hub, demonstrates a commitment to fostering lifelong depositor relationships.

To effectively implement this strategy, financial institutions must innovate by adopting digital-first solutions that appeal to younger generations. Creating a seamless transition from minor to adult accounts captures a high customer lifetime value. By offering co-branded services and advanced learning opportunities through platforms like Life Hub, banks can ensure they remain relevant and competitive against fintech threats. Engaging parents as primary gatekeepers and establishing trust through tailored financial education further solidifies these relationships.

Life Hub's framework offers a compelling model. With its "learn-and-earn" approach, children gain financial literacy while institutions build loyal customer bases. This model also efficiently meets CRA obligations by enhancing access to financial services in underserved communities. According to industry analysis, the payoff of early-life customer engagement translates into a robust long-term financial relationship, a priority for sustainable financial growth.

The operational examples provided by partnerships with institutions like Old National Bank and United Federal Credit Union highlight the Life Hub’s efficacy in community enrichment and business growth. Through real-world applications and measurable outcomes, these partnerships not only meet educational goals but also achieve impressive social returns on investment. Engaging with Life Hub can thus convert regulatory expenses into potent acquisition strategies, delivering significant value.

As we navigate the financial sector's complexities, embracing a holistic approach that integrates technological advancements, youth engagement, and community responsibility is crucial. Financial institutions worldwide are invited to explore how they might capitalize on platforms like Life Hub. By doing so, they can redefine their deposit strategies and cultivate lifelong relationships that benefit both their institutions and the communities they serve. Start transforming today for a resilient tomorrow.

Whether you're parents, or a homeschool family, Life Hub is your partner to help you

raise super strong kids.

Turning high value micro-learning into real-world cash and non-cash rewards with tokenization.

.svg)

Electus Global Education Co, Inc. has received support from The American Heart Association Social Impact Funds.

.svg)