Related Content

No items found.

Banks operate in communities, and communities need support to thrive. The Community Reinvestment Act requires financial institutions to meet the credit needs of the neighborhoods they serve, especially in low- and moderate-income areas. Understanding how cra programs work helps organizations identify partnership opportunities that bring financial education and economic support to young people who need it most.

The Community Reinvestment Act (CRA) became law in 1977 to address discriminatory lending practices. Federal banking regulators evaluate how well banks serve their entire community, not just wealthy customers. These evaluations result in ratings that can influence bank expansion plans and merger approvals.

CRA programs represent the specific initiatives banks develop to meet their community obligations. Banks may offer small business loans, affordable housing financing, or financial education programs. The act encourages institutions to make investments that strengthen local economies.

Banks approach their CRA responsibilities through three main test areas: lending, investment, and service. Each area offers opportunities for supporting youth development and financial capability.

The lending test examines how banks distribute home mortgages, small business loans, and consumer credit across different income levels. Banks earn positive consideration when they lend to underserved populations and support community development.

Investment activities include:

Service activities focus on how banks deliver services throughout their assessment areas. This includes branch locations in low-income neighborhoods, free or low-cost accounts, and financial education programs.

Young people in underserved communities face significant barriers to financial opportunity. They may lack access to banking services, financial education, or mentorship. CRA programs can address these gaps through targeted investments in youth development.

Financial institutions need measurable, impactful programs to demonstrate their community commitment. Youth financial education initiatives offer clear outcomes that satisfy CRA examiners while building real skills.

The Federal Reserve Board emphasizes that banks should partner with community organizations to maximize impact. Youth-serving nonprofits, schools, and community centers understand local needs better than any outside institution.

Effective partnerships require clear goals and accountability. Banks want to fund programs that produce documented results. Organizations need flexible support that reaches young people where they are.

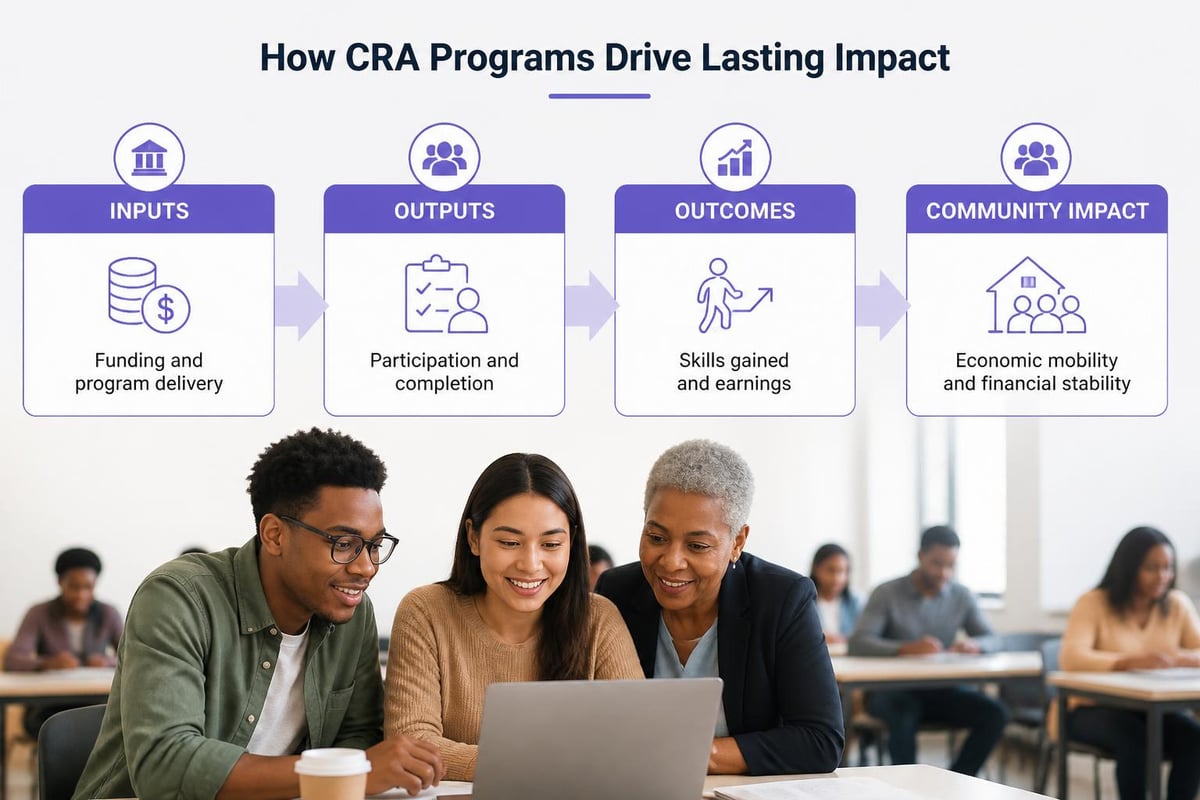

Programs that pay young people for learning create a direct connection between education and economic opportunity. When learners earn money while building skills, banks can track participation rates, completion rates, and economic impact per dollar invested.

Banks structure their community investments in various ways. Some programs focus narrowly on specific outcomes, while others take broader approaches to community development.

Program TypeFocus AreaYouth ImpactFinancial Education GrantsBanking basics, budgeting, savingDirect skill developmentSmall Business SupportEntrepreneurship, business planningCareer pathway exposureTechnology AccessDigital literacy, workforce toolsEmployability skillsScholarship FundsAcademic achievement, college accessEducational attainmentMatched Savings ProgramsSaving behavior, goal settingFinancial capability

Traditional financial education often fails to engage young people. Lectures about compound interest do not create lasting behavior change. Programs that combine learning with earning produce better outcomes.

Banks increasingly recognize that micro-learning platforms deliver measurable results. Short, focused learning tasks fit into busy schedules and maintain engagement. When young people receive immediate compensation for completing financial education modules, participation increases significantly.

This approach aligns perfectly with CRA objectives. Banks can document exactly how many young people gained specific skills and how much economic benefit flowed into the community.

The Federal Reserve Bank of Richmond notes that workforce development programs qualify for CRA consideration when they serve low- and moderate-income individuals. Career readiness programs help young people access better employment opportunities.

Effective workforce programs teach practical skills employers actually need. Microsoft Office proficiency, professional communication, and project management create job opportunities. Programs combining these skills with financial capability prepare young people for economic independence.

Federal regulators expect banks to demonstrate real community benefit, not just check boxes. The FDIC's CRA resources explain how examiners evaluate program effectiveness during CRA examinations.

Banks need data that shows their investments produce results. Strong programs track multiple metrics:

Programs that deposit earnings directly to participants create an automatic audit trail. Every dollar earned represents a completed learning activity and verified skill development.

Many youth programs report "hours of instruction delivered" or "students served" without demonstrating actual learning or behavior change. These metrics satisfy minimal reporting requirements but do not prove community benefit.

Banks operating under CRA programs increasingly demand evidence of real impact. When a young person completes a financial literacy module and receives $5 deposited to their account, the bank can document both the educational outcome and the economic benefit.

Successful cra programs require alignment between financial institutions and community organizations. Both parties bring essential resources to the relationship.

Financial institutions seek organizations that can scale proven programs across their assessment areas. They want partners who understand compliance requirements and can provide required documentation.

Key partnership qualities include:

Organizations working with youth-oriented groups already have community connections and trust. Adding measurable financial education components makes these partnerships more attractive to CRA-focused banks.

The best cra programs serve multiple objectives simultaneously. Young people gain practical skills and earning opportunities. Community organizations expand their reach and impact. Banks meet regulatory requirements while strengthening future customer relationships.

Programs structured around paid learning tasks achieve this balance naturally. Learners build capabilities in 21st century skills including financial literacy, technology proficiency, and critical thinking. Funders can prove exactly how their investment benefited the community.

StakeholderPrimary BenefitSecondary BenefitsYoung LearnersCash earnings, skill developmentConfidence, career awareness, financial toolsCommunity OrganizationsProgram funding, impact metricsMember engagement, documented outcomesFinancial InstitutionsCRA compliance, community investmentCustomer acquisition, brand reputationParents and SchoolsYouth development, financial capabilityReduced family stress, improved academic focus

Banking regulators modernized CRA regulations in 2024 to reflect changes in how people bank. The Federal Reserve Bank of Cleveland explains how these updates affect community investment strategies.

More banks operate across wide geographic areas without physical branches. New regulations recognize digital banking realities and allow institutions to serve communities remotely. This expands possibilities for youth programs that work through mobile apps and web platforms.

Young people already spend significant time on digital devices. Programs delivered through familiar technology reduce barriers to participation. When learners can complete financial education modules on their phones and receive immediate payment, engagement rates increase dramatically.

Regulators increasingly emphasize outcomes over activities. Banks cannot simply write checks to organizations and call it community investment. They must demonstrate that their funding created tangible benefits for low- and moderate-income individuals.

This trend favors programs with built-in accountability. When every program dollar connects directly to a verified learning outcome and measurable payment to a young person, compliance becomes straightforward.

Many young people in underserved communities lack access to basic banking services. Parents may not have bank accounts or may avoid traditional financial institutions. This creates barriers to economic participation that persist into adulthood.

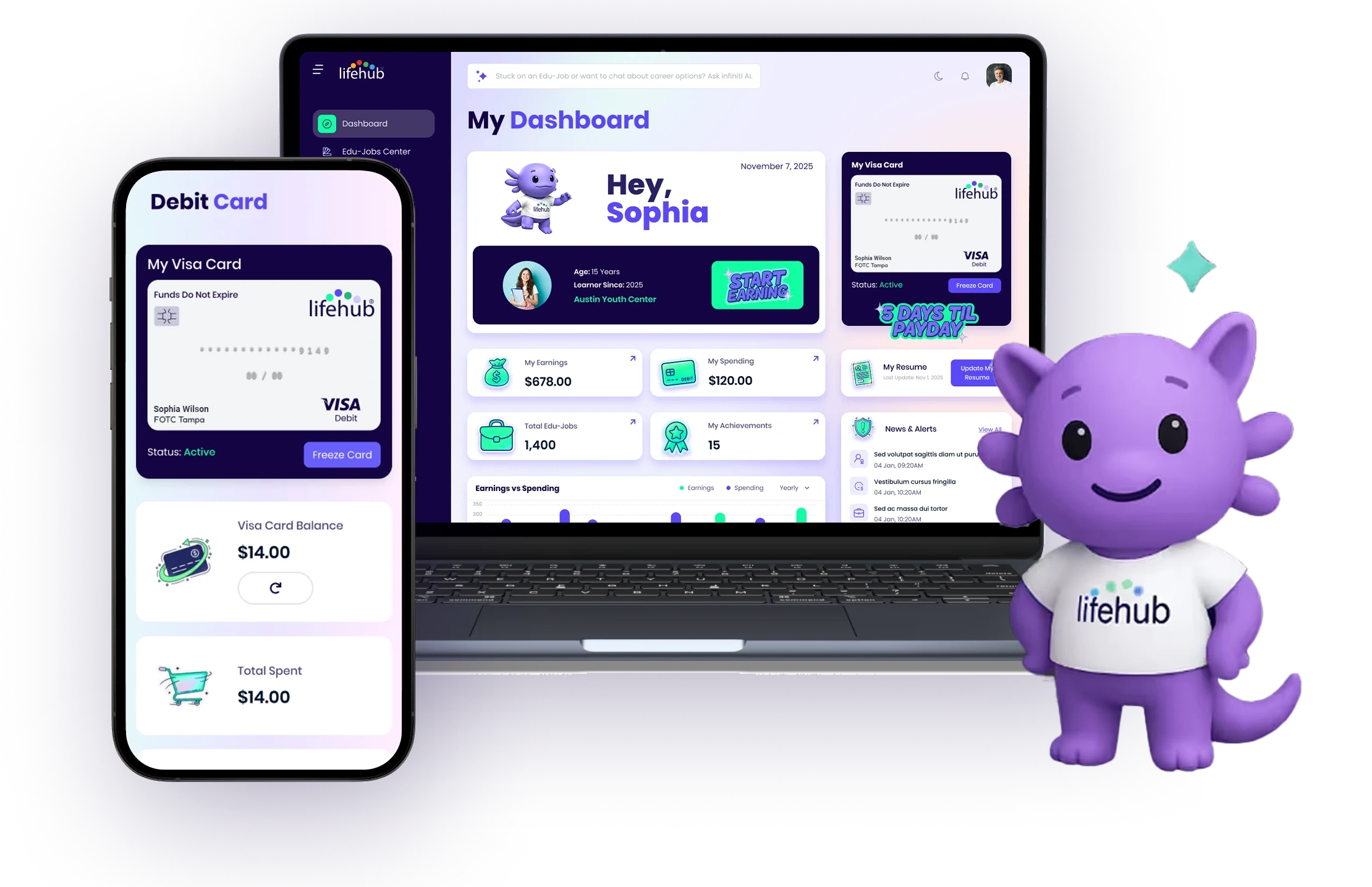

CRA programs that provide young people with their own debit cards introduce them to mainstream financial services early. When learners earn money through educational activities and manage those earnings through proper banking tools, they develop healthy financial habits.

Small pilot programs may show promising results but struggle to reach enough people to satisfy CRA requirements. Banks need partners who can deploy effective programs across entire regions.

Scaling youth financial education requires robust technology systems. Organizations must track thousands of participants, verify learning outcomes, process payments, and generate compliance reports. Manual processes break down quickly as programs grow.

Platforms designed specifically for paid learning can handle these demands. Automated verification, secure payment processing, and comprehensive reporting make large-scale programs manageable.

Programs that scale successfully maintain core effectiveness while reaching more participants. The learning content must remain engaging and relevant. Payment processing must stay reliable and prompt. Support systems must help both learners and program administrators.

This requires careful attention to program design from the beginning. Schools and districts implementing paid learning programs need clear procedures for enrolling learners, monitoring progress, and resolving issues.

Organizations receiving funding through cra programs must understand basic compliance requirements. While banks handle most regulatory obligations, community partners play important roles in documentation and reporting.

Programs serving young people must protect participant information rigorously. Banks need aggregate data about program outcomes but should not receive personally identifiable information about individual learners without proper consent.

Strong programs separate operational data from compliance reporting. Funders receive statistics about participation rates, completion rates, and economic impact without accessing individual learner records.

CRA programs must serve their intended populations without creating inappropriate barriers. Eligibility requirements should focus on income levels and geographic location, not factors that may discriminate against protected groups.

Programs that automatically qualify participants based on school enrollment or community organization membership simplify access while ensuring fair distribution of benefits.

Understanding how cra programs work opens opportunities for organizations supporting youth development in underserved communities. Banks need partners who can demonstrate measurable impact through programs that combine education with economic opportunity. Life Hub provides the platform, payment infrastructure, and learning content that make CRA partnerships successful while building the skills young people need for lifelong financial success.

Whether you're parents, or a homeschool family, Life Hub is your partner to help you

raise super strong kids.

Turning high value micro-learning into real-world cash and non-cash rewards with tokenization.

.svg)

Electus Global Education Co, Inc. has received support from The American Heart Association Social Impact Funds.

.svg)