Choosing the right financial tool for your child can shape how they understand money for years to come. The greenlight vs gohenry debate has dominated family finance discussions since both platforms emerged as leaders in youth banking. Both offer debit cards, parental controls, and educational features, but they take different approaches to teaching financial responsibility. Parents in 2026 want more than just a card. They want tools that build real skills while keeping spending safe and trackable.

What Makes These Platforms Different

Greenlight and GoHenry both provide debit cards designed for minors with parent-managed accounts. Each platform lets parents set spending limits, track transactions in real time, and assign chores or tasks for allowance. The similarities end there.

Core Features Comparison

When evaluating greenlight vs gohenry, the feature set reveals distinct philosophies. Greenlight focuses on investment education and flexible controls. GoHenry emphasizes structured learning modules and charity giving.

| Feature |

Greenlight |

GoHenry |

| Monthly Fee |

$5.99 (up to 5 kids) |

$4.99 per child |

| Investment Options |

Yes (stocks, ETFs) |

No |

| Financial Education |

In-app games, videos |

Structured Money Missions |

| Charity Donations |

Limited |

Built-in giving tools |

| ATM Withdrawals |

Free (up to $25/month) |

$2 fee per withdrawal |

Greenlight's pricing benefits larger families. One subscription covers multiple children, making it economical for parents with three or more kids. GoHenry charges per child, which can add up but provides individual attention to each learner's progress.

The comparison between GoHenry and Greenlight shows that families prioritize different features based on their values and teaching goals.

Setting Up Parental Controls

Both platforms give parents substantial oversight. You can approve or decline transactions before they happen, set spending categories, and block certain merchant types entirely. The greenlight vs gohenry control systems differ in flexibility.

Spending Category Management

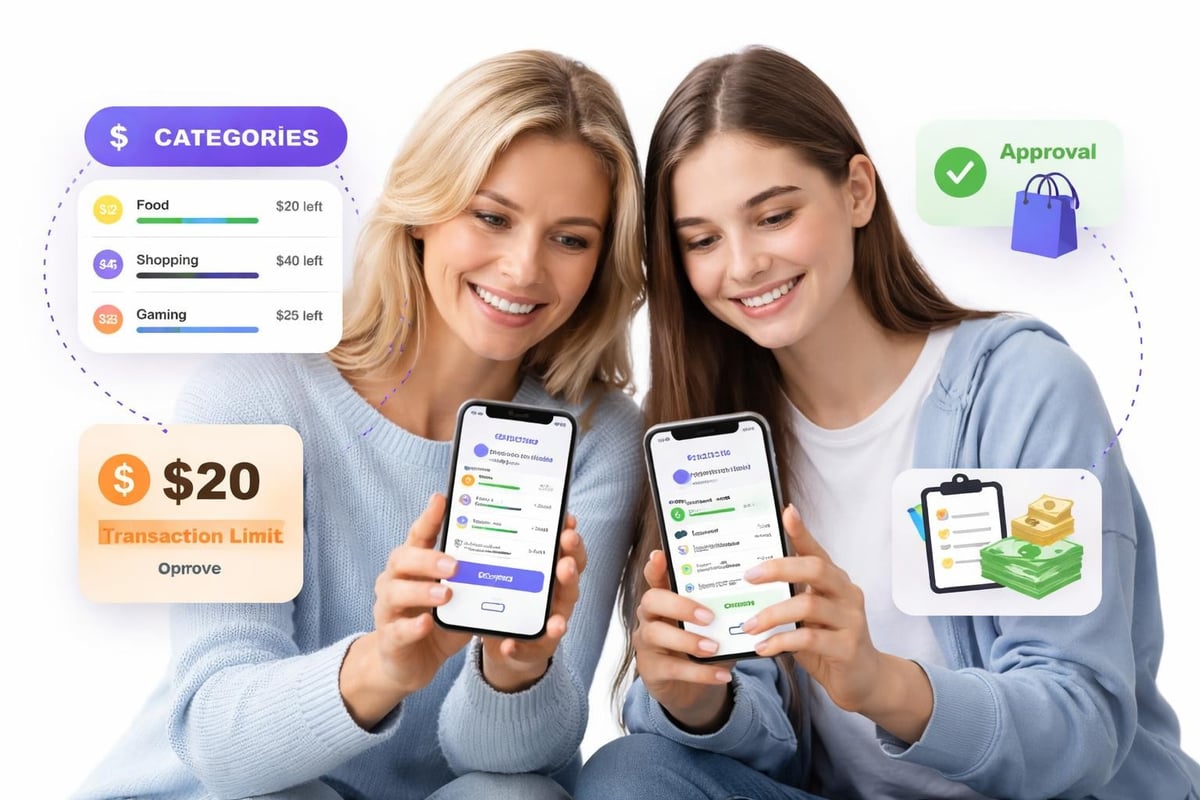

Greenlight allows custom spending categories with individual limits. Parents can create a category called "school lunch" with a $40 weekly limit separate from a "weekend activities" budget of $20. If your child tries to spend lunch money on entertainment, the transaction declines.

GoHenry uses preset spending categories but adds task management directly into the allowance system. Parents assign tasks with specific payment amounts. When a child marks a task complete, parents approve it and money transfers automatically.

Key control features include:

- Real-time spending notifications

- Merchant blocking by category

- Geographic spending limits

- Schedule-based allowance automation

- Transaction approval queues

This level of control helps families teach boundaries without removing all independence. Young people learn to manage within limits rather than facing unlimited access or complete restriction.

Financial Education Approaches

The educational philosophy separates greenlight vs gohenry more than any other factor. Greenlight treats financial education as experiential learning through actual investing. GoHenry structures education as a curriculum with clear progression.

Greenlight's Investment Focus

Greenlight offers fractional shares of stocks and ETFs. Parents maintain approval rights over investments, but children research companies, submit trade requests, and watch their portfolio grow or shrink with market movements. This hands-on approach teaches market dynamics, compound interest, and risk management through real money.

The investment feature requires the Greenlight + Invest plan at $9.98 monthly. For families committed to teaching wealth building beyond spending management, this feature provides tangible lessons that theoretical education cannot match.

GoHenry's Structured Curriculum

GoHenry developed Money Missions, a series of interactive modules covering earning, saving, spending, and giving. Each mission includes videos, quizzes, and activities designed for specific age groups. The review of GoHenry's features highlights how this structured approach appeals to parents who want measurable learning outcomes.

Children earn badges and rewards for completing missions. The gamification keeps younger learners engaged without relying solely on spending their allowance. This can complement programs that combine financial literacy with broader life skills education.

Cost Analysis for Families

Monthly fees represent just part of the total cost picture. The greenlight vs gohenry pricing includes subscription fees, transaction charges, and optional upgrade tiers.

Greenlight pricing tiers:

- Greenlight Core ($5.99/month): Basic card, controls, allowance management

- Greenlight + Invest ($9.98/month): Adds stock investing, retirement savings

- Greenlight Max ($14.98/month): Priority support, identity theft protection, cell phone protection

GoHenry pricing:

- Standard plan ($4.99/month per child): All features included

- Annual plan ($49.99/year per child): Saves approximately $10 yearly

For a family with one child, GoHenry costs less. A family with four children pays $19.96 monthly with GoHenry but only $5.99 with Greenlight Core. The math shifts significantly with family size.

Additional costs matter too. GoHenry charges $2 for ATM withdrawals while Greenlight allows free withdrawals up to $25 monthly. Replacement card fees run $5 on both platforms. International transaction fees apply at 3% for both services.

Teaching Earning and Saving Habits

Both platforms connect tasks to earnings, but implementation varies. In the greenlight vs gohenry comparison, task management shows different strengths.

Chore and Task Systems

Greenlight's task system appears simpler. Parents create a task, assign a value, and set whether it repeats. Children mark tasks complete and request payment. Parents approve with one tap. The system works but lacks detailed tracking of task history or performance patterns.

GoHenry integrates tasks more deeply into the financial ecosystem. The platform tracks completion rates, shows trends over time, and suggests age-appropriate task values. Parents can see which tasks children complete consistently and which they avoid, informing conversations about responsibility and follow-through.

This approach mirrors how micro-learning platforms structure educational tasks with clear objectives, completion tracking, and immediate rewards. The connection between effort and payment becomes tangible when systems provide transparency.

Savings Goals and Automation

Both apps support savings goals with visual progress tracking. Children name their goal, set a target amount, and watch a progress bar fill as they save. Greenlight adds automation features that transfer a percentage of allowance or task earnings directly to savings before children see the spendable balance.

GoHenry's savings visualization includes milestone celebrations and parent matching options. Parents can agree to match savings contributions at a set ratio, teaching how employer retirement matches work in adult finance.

Real-World Money Management

The card experience itself shapes how young people interact with money. Features like spending notifications, balance checks, and merchant acceptance affect daily use.

Card Functionality and Acceptance

Both Greenlight and GoHenry issue cards on major networks (Mastercard for Greenlight, Visa for GoHenry). Acceptance rates remain high at physical stores, online retailers, and digital payment systems.

Greenlight cards work with Apple Pay, Google Pay, and Samsung Pay. GoHenry recently added digital wallet support in 2025. This contactless payment capability reflects how most transactions happen today, preparing young people for cashless commerce.

The range of digital allowance apps available in 2026 shows that card functionality has become table stakes. Differentiation comes from how platforms help families discuss spending decisions, not just enable them.

Transaction Monitoring and Conversations

Real-time notifications create teaching moments. When your child makes a purchase, both you and they receive instant confirmation with merchant name, amount, and remaining balance. This immediate feedback loop helps learners connect abstract digital balances to concrete spending actions.

Parents can leave comments on specific transactions in Greenlight, turning a coffee shop purchase into a discussion about wants versus needs. GoHenry includes spending analytics that categorize purchases automatically, helping families review monthly patterns together.

Privacy, Security, and Account Safety

Financial tools for minors carry particular security responsibilities. The greenlight vs gohenry security comparison shows robust protection on both sides.

Security features both platforms provide:

- 256-bit SSL encryption

- Two-factor authentication for parent accounts

- Instant card locking through the app

- Zero liability for unauthorized transactions

- FDIC insurance through partner banks

Neither platform checks credit or affects credit scores since these are prepaid debit cards, not credit products. Parents load funds that children spend. No overdrafts, no debt, no credit reporting.

GoHenry maintains offices in both the US and UK, complying with financial regulations in both markets. Greenlight operates under US regulations exclusively. Both platforms have established track records, with customer reviews indicating general satisfaction with security measures.

Age Appropriateness and Growth Potential

Children's financial needs evolve from elementary school through high school. The greenlight vs gohenry platforms serve different age ranges with varying effectiveness.

Elementary School Learners

GoHenry's structured Money Missions work well for younger children (ages 6-10) who benefit from clear progression and visual rewards. The tasks remain simple and the educational content uses age-appropriate language and concepts.

Greenlight serves this age group adequately but shines less brightly. The investment features may overwhelm younger learners who lack context for stock markets and compound interest.

Middle and High School Learners

As children enter their teens, Greenlight's sophisticated features become more relevant. The ability to invest small amounts in real companies, learn about market volatility, and build a portfolio teaches lessons that structured courses cannot replicate.

GoHenry remains useful but may feel limiting to older teens who want more financial autonomy. The platform's safety-focused design, perfect for younger children, can frustrate 16-year-olds ready for more independence.

This progression mirrors broader educational journeys where life skills curricula adapt to developmental stages, introducing complexity as learners gain capability.

Additional Features Worth Considering

Beyond core banking and education features, each platform includes extras that may influence your decision.

Greenlight Unique Features

The Greenlight Max tier adds identity theft protection and cell phone insurance. While marketed to teens, these features protect the whole family. Cell phone protection covers up to $600 in repair or replacement costs after a $50 deductible, which can pay for the higher subscription tier if your teen damages their phone.

The platform also includes location-based notifications. Parents receive alerts when their child uses their card near specific locations like school, work, or designated stores. This geofencing capability adds safety monitoring beyond financial tracking.

GoHenry Unique Features

GoHenry's charity giving integration stands out. Children can donate directly from their account to verified charities through the app. The platform provides age-appropriate information about charitable organizations and tracks giving history, teaching philanthropy alongside personal finance.

The video feature in Money Missions uses relatable scenarios rather than abstract concepts. Children watch situations like saving for a concert ticket or deciding between two purchase options, then answer questions about the decisions made.

Support and Customer Experience

When issues arise, response time and solution quality matter. Both platforms offer support through multiple channels.

| Support Feature |

Greenlight |

GoHenry |

| Email Support |

Yes |

Yes |

| Phone Support |

Yes (Max tier priority) |

Yes |

| Live Chat |

Yes |

Limited hours |

| Help Center |

Extensive |

Comprehensive |

| Average Response Time |

24-48 hours |

12-24 hours |

User reviews on Trustpilot indicate that both platforms handle common issues like card activation, transaction disputes, and account access problems effectively. Response times vary by issue complexity and support tier.

The Greenlight Max subscription includes priority support with faster response times and dedicated assistance. For families managing multiple children or complex allowance structures, this may justify the higher cost.

Integration with Family Financial Goals

The greenlight vs gohenry decision should align with your broader approach to raising money-smart kids. Consider these questions:

What financial behaviors do you want to encourage?

If saving and giving matter most, GoHenry's goal tracking and charity features align well. If investing and wealth building top your priorities, Greenlight's stock market access provides hands-on education.

How much parental involvement do you prefer?

Both platforms require initial setup, but ongoing management differs. Greenlight's automation features reduce weekly involvement. GoHenry's structured missions work better when parents engage with the content alongside their children.

What's your family's learning style?

Experiential learners thrive with Greenlight's real-world investing. Children who prefer guided instruction may engage more with GoHenry's curriculum approach. Neither method is superior, just different.

Making the Choice for Your Family

The greenlight vs gohenry comparison reveals two quality platforms with distinct strengths. Greenlight offers sophistication, flexibility, and investment education. GoHenry provides structure, charity integration, and age-specific content.

Your decision factors might include:

- Number of children (impacts per-child cost)

- Age range (younger kids vs. teens)

- Educational philosophy (hands-on vs. structured)

- Specific features (investing, charity, task management)

- Budget considerations (monthly fees, transaction costs)

Both platforms deliver on their core promise of safe, parent-controlled spending combined with financial education. The "better" choice depends entirely on your family's unique needs and values.

Some families use both platforms sequentially, starting younger children on GoHenry's structured program and transitioning to Greenlight as they enter high school and seek investment opportunities. Others commit to one platform and maximize its features across all age ranges.

Beyond Basic Banking Tools

While dedicated debit cards serve an important role, comprehensive financial education extends beyond spending management. Young people need exposure to earning through work, understanding how skills translate to income, and building confidence in their ability to create value.

The greenlight vs gohenry conversation focuses primarily on spending and saving. Real financial capability includes earning potential, career exploration, and connecting education to economic outcomes. Tools that integrate financial literacy with practical skill building prepare young people for economic independence more completely than spending controls alone.

Whether you choose Greenlight, GoHenry, or another platform, prioritize ongoing conversations about money. The technology enables tracking and education, but human discussion builds understanding. Talk about spending decisions, saving trade-offs, and long-term goals. Review transactions together weekly. Celebrate savings milestones. Discuss investment gains and losses without judgment.

Financial education works best when it combines practical tools with supportive guidance. The greenlight vs gohenry platforms provide the tools. You provide the guidance that turns features into lasting lessons.

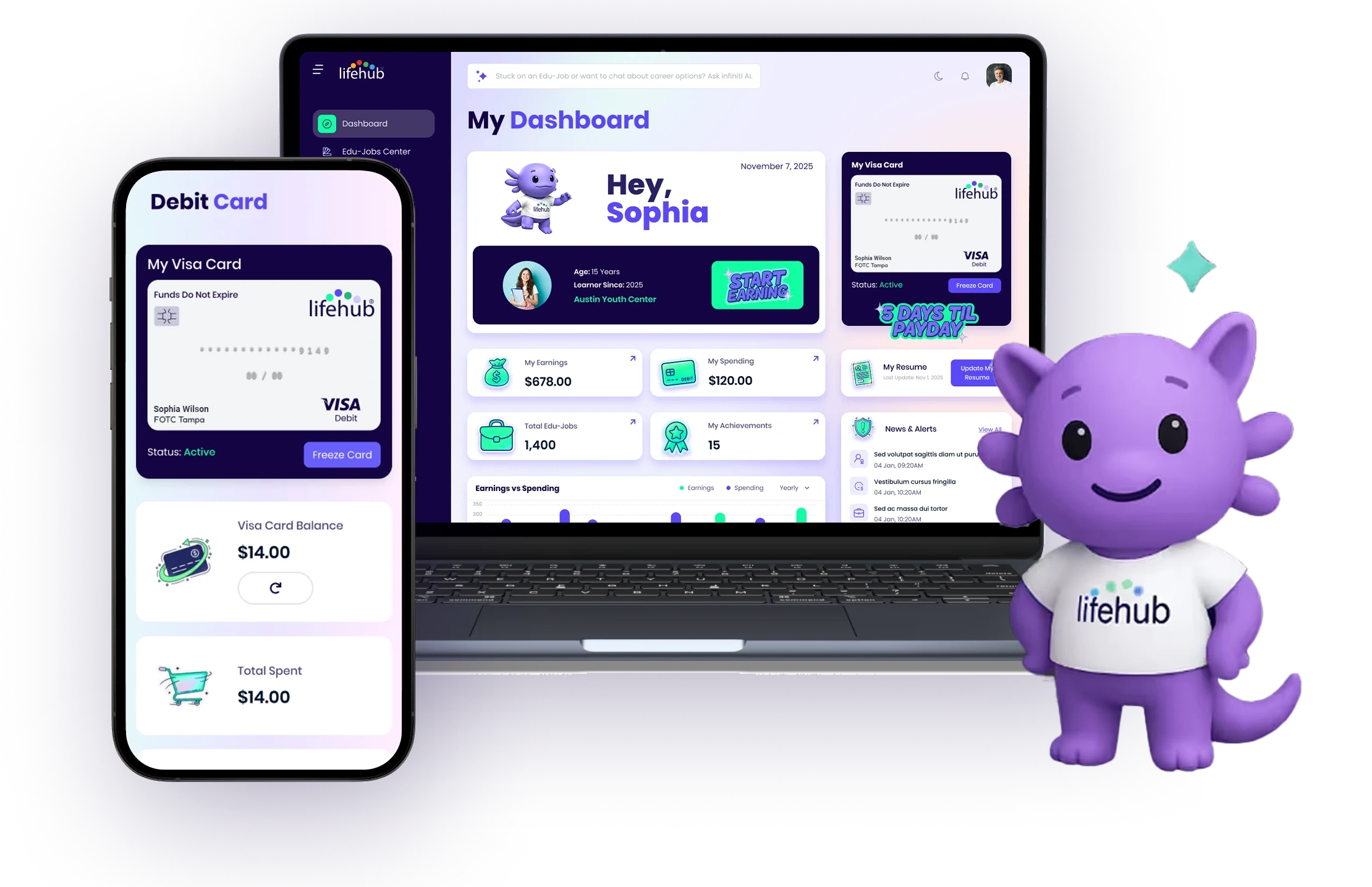

Both Greenlight and GoHenry offer valuable features for teaching money management through hands-on experience with real spending decisions. The right choice depends on your family's size, values, and learning style. If you want to go beyond basic spending controls and help young people build comprehensive financial capability through earning, Life Hub connects practical skill development with real compensation. Learners complete micro-learning tasks across financial literacy, academics, career readiness, and digital skills while earning money that flows to their own debit card, creating a direct link between capability building and economic reward.

.avif)

.png)

.svg)

.svg)