The Greenlight debit card has become one of the most popular tools for parents who want to teach their children about money management. Since launching several years ago, Greenlight has helped millions of families introduce financial concepts through real-world practice. This card gives young people a safe way to spend, save, and learn while parents maintain oversight and set appropriate boundaries. Understanding how Greenlight works can help you decide whether it fits your family's financial education goals.

What Makes the Greenlight Debit Card Different

The Greenlight debit card functions as a reloadable prepaid card designed specifically for children and teenagers. Greenlight's official documentation confirms that it operates on the Mastercard network, meaning it works at most retailers, ATMs, and online merchants. Parents control the card through a mobile app where they can instantly transfer money, set spending limits, and monitor every transaction.

Unlike traditional bank accounts, Greenlight offers features built around parent-child money conversations. The app allows you to assign chores with attached payment amounts. When children complete tasks, parents approve them and release funds directly to the card. This creates an immediate connection between work and earnings.

Core Features and Controls

Parents can create up to five cards per subscription. Each child gets their own card with customized controls:

- Spending categories: Block or allow specific merchant types like restaurants, gas stations, or online shopping

- Store-level controls: Approve or deny spending at individual stores

- ATM access: Enable or disable cash withdrawals

- Real-time notifications: Receive alerts when your child makes a purchase

- Transaction history: Review all spending with merchant names and locations

The app also includes savings goals where children can allocate money toward specific targets. Parents can set interest rates on savings to demonstrate how money grows over time. Some families use this feature to match contributions, doubling their child's savings when they reach milestones.

Pricing Plans and Cost Structure

Greenlight offers three subscription tiers with different feature sets. All plans include basic money management tools, but higher tiers add investment and identity protection features.

| Plan |

Monthly Cost |

Cards Included |

Key Features |

| Greenlight Core |

$5.99 |

Up to 5 |

Basic spending controls, chore management, savings goals |

| Greenlight Max |

$9.98 |

Up to 5 |

Core features plus investment account, identity theft protection, cell phone protection |

| Greenlight Infinity |

$14.98 |

Up to 5 |

Max features plus 5% cash back (up to $100/month), shopping protection, travel benefits |

BestMoney's comprehensive analysis notes that Greenlight charges no transaction fees, overdraft fees, or monthly inactivity fees. However, ATM withdrawals at out-of-network machines typically cost $2.50 plus any additional fees from the ATM operator.

The subscription cost covers the entire family regardless of how many children you have. If you have four kids, you'll pay the same monthly fee as someone with one child. This makes the per-child cost more reasonable for larger families.

Hidden Costs to Consider

While Greenlight advertises no hidden fees, some activities do trigger charges:

- Replacement cards cost $3.50 each

- Expedited shipping for new cards adds extra fees

- International transactions may include conversion fees

- Same-day transfers carry a 1.5% fee with a $3 minimum

Most families can avoid these costs through normal use. The base subscription price remains the primary ongoing expense.

How Greenlight Compares to Other Options

The youth banking market has grown significantly since 2020. FinanceBuzz's evaluation compares Greenlight against competitors like GoHenry, FamZoo, and BusyKid. Each platform takes a different approach to financial education.

Greenlight stands out for its intuitive interface and comprehensive parental controls. The app receives regular updates and maintains strong security standards. However, the monthly subscription may feel expensive compared to free checking accounts offered by traditional banks.

Some families prefer debit cards designed to work alongside educational programs that actively teach financial concepts rather than just providing spending tools. The best choice depends on whether you want passive monitoring or active learning experiences.

Strengths and Limitations

What Greenlight does well:

- Clean, user-friendly mobile app for both parents and children

- Flexible controls that grow with your child

- Integration with chore tracking and allowance management

- Strong customer support through multiple channels

- Regular feature updates based on user feedback

Where it falls short:

- Monthly fees add up over time (approximately $72-$180 annually)

- No interest paid on savings in the basic plan

- Investment features require higher-tier subscriptions

- Some parents find the controls overly complex initially

- Limited educational content within the app itself

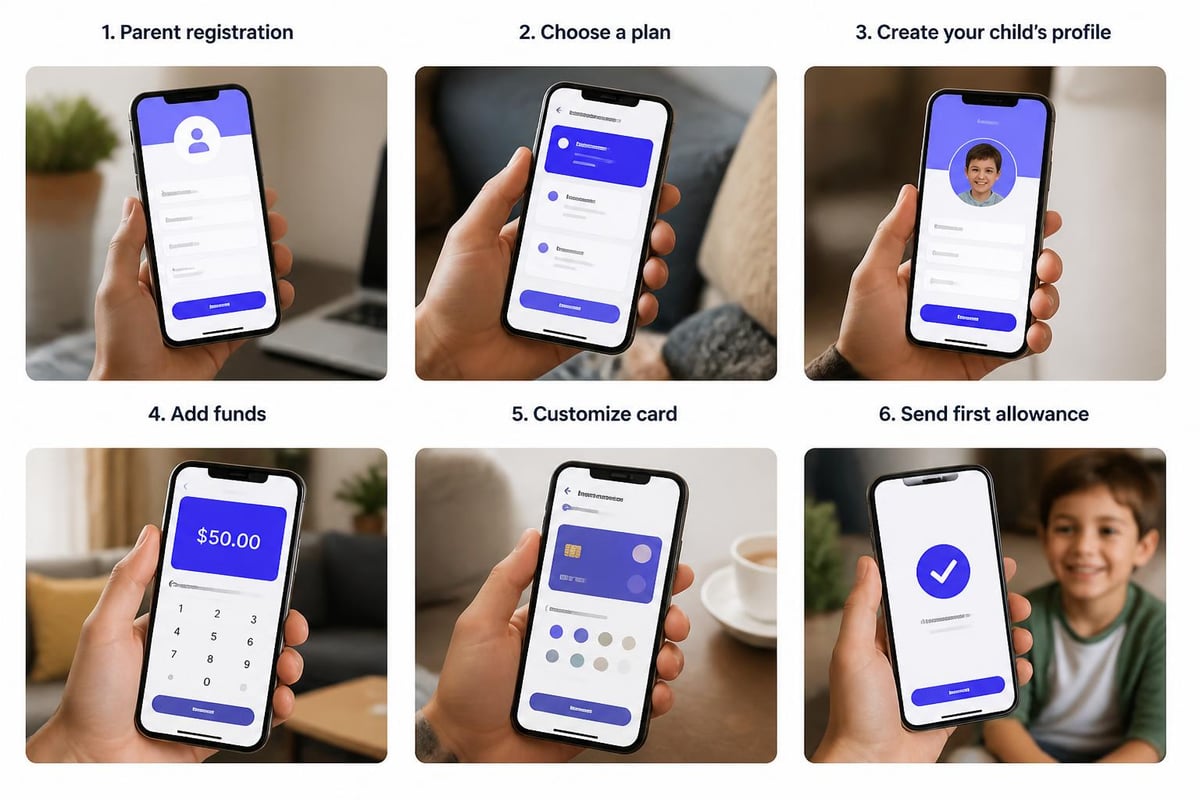

Setting Up and Using the Greenlight Debit Card

Getting started with Greenlight takes about 10 minutes. Parents download the app, create an account, and enter payment information for the monthly subscription. Children's profiles require basic information including name and birthdate.

Physical cards arrive within 7-10 business days. While waiting, parents can set up the account structure, configure controls, and transfer initial funds. Children can also download the app to explore their interface before the card arrives.

Teaching Moments with Greenlight

The platform works best when parents use it as a conversation starter rather than just a payment method. Kids' Money shares practical experiences showing how families integrate Greenlight into regular financial discussions.

Consider these approaches:

- Weekly money meetings: Review spending together and discuss choices

- Goal-setting sessions: Help children define what they're saving toward

- Budgeting practice: Allocate allowance across spending, saving, and giving

- Mistake analysis: When overspending happens, talk through what went wrong

These conversations matter more than the card itself. Technology provides data and convenience, but parents provide context and wisdom. The most successful Greenlight users combine the tool with consistent financial education.

Security and Safety Features

Greenlight clarifies its security approach through multiple protective layers. The card carries zero liability for unauthorized transactions, meaning families won't lose money if the card is stolen or compromised.

Parents receive instant notifications for every transaction. If suspicious activity appears, you can immediately freeze the card through the app. This prevents further unauthorized use while you investigate. New cards can be ordered quickly if needed.

Account Protection Measures

Greenlight employs bank-level encryption to protect account data. The company is not a bank itself but partners with Community Federal Savings Bank. Funds are FDIC-insured up to $250,000 per account.

Additional security features include:

- Biometric login (fingerprint or face recognition)

- Two-factor authentication for account access

- Automatic logout after inactivity

- Secure card lock/unlock toggle

- Fraud monitoring on all transactions

The app never stores full card numbers on mobile devices. Even if someone gains access to your phone, they cannot see complete payment information.

Real-World Applications and Learning Opportunities

Greenlight creates natural opportunities for financial education through daily experiences. When children want to purchase something, they check their balance first. This simple act builds awareness of available resources.

The spending category controls introduce the concept of budgeting. You might give a child $50 for the month with limits on entertainment spending. They learn to prioritize within constraints, a skill that transfers to adult budgeting.

Finder.com's review highlights how families use the platform for different age groups. Younger children (6-10) typically focus on earning allowance through chores and basic spending decisions. Teenagers (13-17) might manage larger amounts while learning about savings interest and investment basics.

Age-Appropriate Money Skills

| Age Range |

Primary Focus |

Greenlight Features to Emphasize |

| 6-9 years |

Earning and spending basics |

Chore assignments, parent approval for purchases, savings goals |

| 10-12 years |

Budgeting and saving |

Weekly allowance allocation, category limits, interest on savings |

| 13-15 years |

Independence and planning |

Store-level controls, ATM access, parent-paid interest, investment intro |

| 16-18 years |

Advanced concepts |

Investment account, job income deposits, college savings, financial independence prep |

Alternatives Worth Considering

While Greenlight offers comprehensive features, other platforms may better fit specific family needs. WalletGrower's comparison examines several alternatives with different pricing structures and educational approaches.

Traditional bank accounts for minors often cost nothing but provide fewer learning tools. Credit unions sometimes offer teen checking accounts with parental oversight at no monthly fee. These work well for families comfortable creating their own financial education curriculum.

Some platforms focus specifically on connecting learning with earning. Programs that integrate education with financial rewards create stronger motivation than passive allowance distribution. Young people engage more deeply when they see direct connections between effort and compensation.

Making the Right Choice

Consider these factors when evaluating youth financial tools:

- Your teaching style: Do you want a hands-on platform or simpler monitoring?

- Budget constraints: Can you sustain monthly fees for multiple years?

- Child's age and maturity: Does your child need basic or advanced features?

- Educational priorities: Do you want passive tools or active learning integration?

- Family size: Will per-family pricing work better than per-card pricing?

The right answer varies by household. Some families rotate through different platforms as children grow. Others stick with one system from elementary school through high school.

Common Parent Questions and Concerns

Parents frequently ask whether Greenlight actually teaches financial responsibility or just enables spending. The honest answer is that the card itself is neutral. Outcomes depend entirely on how families use it.

Without parental engagement, Greenlight becomes just another way to give kids money. The real value emerges through conversations about purchases, discussions of savings goals, and analysis of spending patterns together.

Tax Implications and Record Keeping

Money transferred to children through Greenlight doesn't typically create tax obligations. Allowance and chore payments are considered gifts rather than income. However, if teenagers use Greenlight for job earnings, those amounts may need to be reported depending on total annual income.

The app maintains complete transaction history, which helps during tax season if needed. You can export data for record keeping or accounting purposes. This feature also helps older teens track income from part-time jobs deposited to their cards.

Integration with Broader Financial Education

Greenlight works best as one component of comprehensive financial education. Schools and organizations that teach life skills recognize that practical money management requires multiple learning experiences over time.

The card provides hands-on practice, but young people also need conceptual understanding. Topics like compound interest, credit scores, investment basics, and budgeting strategies require explanation beyond what any app provides.

Many families combine Greenlight with other educational resources. Books, online courses, family discussions, and structured learning programs all contribute to financial literacy. The debit card gives children a laboratory for applying concepts they learn elsewhere.

Building Toward Financial Independence

The ultimate goal is preparing young people to manage money independently. Greenlight can support this progression by gradually increasing freedom and responsibility. Parents might start with strict controls for younger children, then slowly remove restrictions as competence grows.

By age 16 or 17, many teenagers use their Greenlight card almost like an adult debit card. Parents maintain oversight but rarely intervene. This transition period builds confidence before young people open their own accounts.

Some families keep Greenlight active even after children leave home. College students may appreciate having parents able to send money quickly or monitor spending during the adjustment to campus life. The flexibility supports families through multiple life stages.

Monthly Costs Versus Long-Term Value

Spending $72-$180 annually on a financial education tool requires justification. Is Greenlight worth the ongoing expense? North State Bank's overview suggests the value depends on family engagement and alternatives.

If Greenlight prompts regular financial conversations and helps children develop better money habits, the cost may deliver significant returns. Poor financial decisions in young adulthood can cost thousands of dollars through overdraft fees, credit card debt, and missed savings opportunities.

However, if the card sits unused or becomes just an electronic allowance transfer system, the subscription provides little value. Free alternatives can accomplish basic money transfers without monthly fees. The premium lies in active use of educational features and parental controls.

The Greenlight debit card offers a structured approach to youth financial education with comprehensive parental controls and practical spending experience. Success depends on family engagement and consistent use of the platform's features. While monthly costs may add up over time, the right tool combined with active teaching can build money skills that last a lifetime. If you're looking for a more comprehensive approach that combines financial education with earning opportunities, Life Hub helps young people build money skills through paid micro-learning tasks across personal finance, entrepreneurship, and real-world capability. Learners earn real cash for completing educational challenges and developing practical competencies, with earnings deposited directly to a Life Hub Visa debit card that turns every dollar into proof of progress and achievement.

.avif)

.png)

.svg)

.svg)